By Ben Kaufman | February 28, 2022

From January 13 to February 15, 2022, the CEO of the tech sales training bootcamp Prehired filed 290 lawsuits—all in Delaware state court, although the defendants live all across the country—demanding former students pay $25,000 apiece on defaulted student loans. Prehired had previously guaranteed to prepare students for and place them in high-paying jobs as sales development representatives, and it had asked students to take on massive student debt along the way using a fringe form of credit called an “Income Share Agreement” (ISA). This debt would cost borrowers 12.5 percent of their gross monthly income up to total payments of $30,000, and it could follow them for up to eight years. That might seem like a hefty set of obligations to take on for a 6-week online class, but Prehired assured students not to worry—after all, the school asserted that the design of the ISA would “align the institution’s success with their members’ success,” helping ensure that the program involved “No Risk.”

Now, those students have 15 or fewer days left to respond to the school’s lawsuits, or they will potentially face default and collection on $25,000 of ISA debt.

This story is yet another unfortunate chapter in the ongoing saga of predatory for-profit vocational bootcamps exploiting the lawlessness of the ISA market to defraud the public—and it is one more flashing signal that law enforcement at all levels must act to reign in this product and the scam schools that rely on it. Just like a long line of financially ruined bootcamp students before them, Prehired’s pupils were lured in by a charismatic founder’s lofty tales of lucrative work in tech and the promise that their ISAs would ensure that their school had their best interests in mind. These students then received an educational product that fell far short of what was marketed, with advertised jobs and mentorships—let alone six-figure salaries—proving illusory. And by the time anyone could realize the depth of this fraud, the school was laughing all the way to the bank, as it had already leveraged the smokescreen of positive rhetoric and novelty surrounding ISAs to lock students into usurious debt contracts.

Schemes like this one have been executed far too many times before by well-funded fraudsters, who use short-term credentialing programs, flashy tech branding, and the positive spin they are able to place on the ISA product to draw vulnerable people into costly private debts. Despite federal and state efforts to rein in the ISA market these rackets depend on, it is clear that they have only continued.

It is long past due for policymakers, regulators, law enforcement, and Congress to hold ISA providers and the bootcamps that rely on them accountable, and to protect borrowers from these predatory shams. Until officials act, the parade of shocking abuses in the ISA and bootcamp markets that these 290 lawsuits exemplify will only continue.

Prehired Used ISAs to Lure in Students, Promising Aligned Incentives

Prehired was founded in 2017 by Joshua Jordan, who had previously started a now-defunct software sales firm. He was soon joined by his brother Caleb, an alleged pedophile who works as Prehired’s current Director of Sales Enablement. Joshua detailed in a 2017 blog post that Prehired offers an “online bootcamp to train sales reps with high aptitude, attitude, and ambition to be the top producers in sales development. . . . [that] also helps these sales reps get hired at software companies around the country.” Prehired now describes itself as “a sales community” that provides “training, mentoring and networking to help you land a full-time sales job in a business-to-business (B2B) software company.”

Central to Prehired’s marketing pitch and business strategy is the idea that students do not pay for its program up front, but instead agree to hand over periodic “membership dues” in the form of an Income Share Agreement. ISAs are a dubious variety of private student loan that requires students to pledge a portion of their future income in exchange for tuition financing. Ideally, this could mean that ISAs are valuable for schools only to the extent that students go on to secure high-earning jobs. However, the Student Borrower Protection Center (SBPC) has long warned that ISAs are risky, expensive, riddled with contractual tricks and traps, and frequently used as the basis for the business models of predatory tech-focused bootcamps.

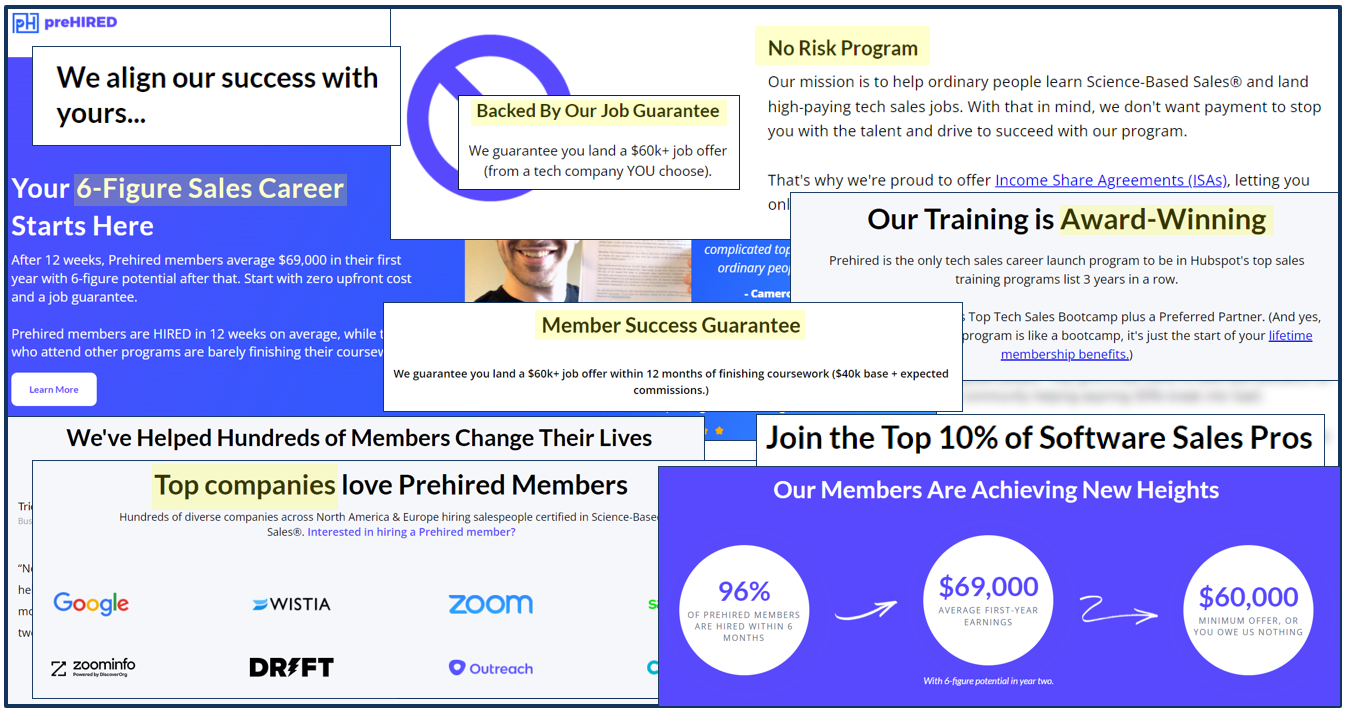

Prehired used lofty promises to draw students into predatory ISAs. Highlights added.

Under Prehired’s ISA—managed by the for-profit ISA provider Meratas, the same company that entered into a consent order in August with California law enforcement regarding misconduct in the ISA space—students with annualized earnings above $60,000 pay 12.5% of their gross income each month for 48 months to cover the cost of their education. If the borrower’s annualized income falls below $60,000 in a given month, they do not owe anything that month. The debt is extinguished at the sooner of the borrower making 48 payments, the borrower making payments that cumulatively reach a $30,000 “cap,” or 8 years passing in the borrower’s repayment sequence (regardless of how many payments the borrower has paid by that point or how much they have paid).

Prehired touts that its use of ISAs allows it to “align our success with yours,” claiming in marketing materials that “[o]ur members only start paying dues only after they land a job and make enough money per month” (emphasis in original).

The student success that Prehired promises is substantial. The company’s website claims that “members average [incomes of] $69,000 in their first year with 6-figure potential after that,” that “96%” of Prehired members are hired within six months, and that “Prehired members are HIRED in 12 weeks on average.” (Notably, the company claims elsewhere that “Members average $73,000 in their first year & 6-figure potential in their second year” [emphasis added], and that students need only work for “3-9 months before a 6-figure income potential” [emphasis added].) In addition, under the header “Top companies love Prehired Members” on a page on its website, Prehired displays the logos of prominent tech firms such as Google and Zoom.

Prehired even advertises a “Member Success Guarantee” stating, “We guarantee you land a $60k+ job offer within 12 months of finishing coursework ($40k base + expected commissions.)” This guarantee appears to be a reference to the ISA, as students would ostensibly not owe the school any money under the ISA if they were not earning $60,000 per year. However, even the “simplified explanation” of this guarantee on Prehired’s website involves no fewer than 3 asterisks pointing to fine print. A full explanation of the guarantee is not publicly available, but Prehired pares back even this simplified description elsewhere on its website, stating there only that “We guarantee you get at least one offer for $60,000+ (with at least $40,000 from base salary)*” (emphasis added).

Prehired’s Program Proved Worthless—But Students were Already Locked into Unaffordable ISAs

A growing wave of student narratives appears to indicate that Prehired’s program is of much lower quality and offers far fewer job prospects than the company advertises and that the ISAs that helped draw students in, have proven to be a particularly predatory form of student debt.

Complaints from students accusing Prehired of being a “scam” have periodically appeared on social media for years, but the dam of harrowing borrower narratives broke soon after the school filed the lawsuits discussed above. After that, former students took to LinkedIn—a common congregating place for those in the sales industry—to describe their true experiences with Prehired. In these students’ telling, both promises of a high-quality education through Prehired and of protection from financial downside through the company’s ISA proved devastatingly hollow.

Student narratives posted to Linkedin included the following:

I had to file bankruptcy. . . . Nothing I’ve ever used in any sales role since has been from PreHired.

Source

When I started my time with PreHired, I was promised the dream of having a 6-figure income. . . . I completed the training in about 2 weeks, started my career search journey and applied to 50+ job postings as I was instructed. None reached out to schedule more interviews. . . . Nearly 2 years later I still do not make close to 6-figures. I have exhausted my savings to keep me afloat but I am just ashamed to have gone through PreHired’s training bootcamp.

Source, emphasis added

I was a former school teacher desperate to change careers during COVID. . . . I was angry when I realized [the training] was pre recorded and that there was no one really there to help you along the way. The job I got approached me because of my degree in business and not because of PreHired. They were not even familiar with them. I was even more angry when I realized that no matter what the training PreHired offered as ‘like nothing else’ was only a blip of the training you get PAID to do during your onboarding process with the company. Absolutely a predatory company.

Source, emphasis added

At the start of COVID I started to search for a work-at-home option in a different field. That night I found a Facebook ad for Prehired. I went through the orientation and the training and then went straight for the mentor job search part of the program. For the next 12 months, I was submitting twice the required applications a week and went on countless interviews but never got a job, except for a job my mentor told me to take that was purely on a commission that only lasted a week, and then the search was back on. Through all this time I was going to physical therapy for a car accident, walking with a cane, going to interviews, caring for a 13-year-old foster son, and burning through all the savings I had. After six months I tried to bow out of the program free of charge but I was told by my mentor that I don’t qualify for that even though it said that on the website and still does. His explanation was that I was late to our zoom meeting twice because I was taking care of a 13-year-old foster son and he was going through some major depressive episodes. . . . Please learn from this and stop destroying other peoples lives.

Source, emphasis added

I signed up for prehired at a time I did not have a job and was desperate while being a college student. . . . Due to the inconsistency in the program, I ended up finding job in my field and tried to talk to Josh about leaving the program because it did not benefit me and I found a job in the current field I worked in, he refused to work with me, he told me that I was indebted for 30k. . . . The practices of Prehired are predatory and take advantage of people when they are at their lowest. I signed up for prehired because I believed in their mission, only to get screwed and now have a threat of a lawsuit over my head in the middle of pandemic. That is not right at all.

Source, emphasis added

These stories appear to be the tip of the iceberg. Students report being instructed to misrepresent their income as being higher than it actually was so that Prehired could increase payments on students’ ISAs, being sent into collections even after being declared 100 percent disabled, and learning after graduation that comparable courses of study are available for free online. Students claim that course modules that they were told would be available in perpetuity are now blocked off, that students were directed to astroturf the web with positive reviews for the course, and that students seeking protection under Prehired’s employment guarantee are systematically given the runaround. Many of these students appear to be military veterans.

The 290 lawsuits that Prehired filed targeted students who were unwilling or unable to continue paying on their ISAs, though both varieties of students generally attribute their non-repayment to Prehired’s broken promises.

Perhaps most damningly, one student who refused in protest to pay on his ISA and who went on to found his own software sales staffing business reports that Joshua Joseph hired him to threaten students with lawsuits if they did not pay on their Prehired ISAs, adding that he “received a lecture from Joshua Jordan on the dynamics of using fear within business tactics.”

Borrowers Deserve Protection from the Ongoing Flood of Predatory ISAs and Unscrupulous Bootcamps

The present revelations about Prehired are just the latest example of the new generation of for-profit schools wrapping predatory debt and meaningless credentials in the language of disruption. After years of periodic headlines about fly-by-night bootcamp operators following the same ISA-based playbook at students’ expense, it is clear that sweeping action is necessary to protect borrowers.

This action clearly must begin with the Consumer Financial Protection Bureau (CFPB), which has expansive authority to monitor, investigate, and conduct enforcement action against anyone providing a “consumer financial product or service.” The Bureau has already taken the first steps to flex this authority to reign in bad practices in the ISA market. To the extent that they are involved with arranging ISA debt for students, bootcamps likely also fall within the CFPB’s ambit. The CFPB must immediately use its broad data collection powers to fully audit and develop an understanding of the ISA market, the bootcamp space, and these two industries’ interaction, and then use its supervision and enforcement authority to weed out bad actors and practices. Developing a deep understanding of this space is a key first step to spotting and preventing future frauds.

[perfectpullquote align=”right” bordertop=”false” cite=”” link=”” color=”” class=”” size=””] Right now, even the least sophisticated of scammers can readily throw together a splashy-seeming tech bootcamp, raise funds for it, and partner with an outside firm to trap students into exploitative ISA financing, all with little threat of legal recourse. [/perfectpullquote]

Congress must also step in. As the SBPC has written before, rules that the Federal Reserve Board wrote in 2008 to implement the Truth in Lending Act (TILA) in the context of student loans are so narrow as to leave huge swaths of students unnecessarily at risk. In particular, while TILA offers strong protections for some private student loan borrowers, those rules do not currently apply to students at many of the riskiest, short-term, unaccredited programs—including many coding bootcamps. Congress can easily fix this by passing the proposed Private Student Loan Parity Act, a bill that would amend TILA to ensure that students enjoy the same high level of protection on their private student loans regardless of what type of program they choose to attend. These protections would vastly improve the public’s ability to identify and prevent scams and to hold the next Joshua Jordan accountable.

But the Bureau, Congress, and partners across state and federal governments must act quickly. It is no exaggeration to say that right now, even the least sophisticated of scammers can readily throw together a splashy-seeming tech bootcamp, raise funds for it, and partner with an outside firm to trap students into exploitative ISA financing, all with little threat of legal recourse. Even when operating without a license, and even after being reprimanded for doing so, bootcamps have systematically been given little more than a slap on the wrist. Plus, when borrowers try to seek justice through the courts, they often find that fine print in their ISA contracts mean their only option is back-door, lopsided arbitration.

This cannot continue to be the case. The example of Prehired shows that the mix of ISAs and for-profit bootcamps continues to produce uniquely horrifying outcomes for students. Instead, it is time for a concerted campaign to protect ISA borrowers.

###

Ben Kaufman is the Director of Research & Investigations at the Student Borrower Protection Center. He joined SBPC from the Consumer Financial Protection Bureau where he worked on issues related to student lending.