People Cheer for Bad Policy, Show Off Their Bad Judgment

By Mike Pierce | April 8, 2026

Last week in Washington (and on the slice of the Internet where think tankers gather), something broke. Some of the very worst and most shameless cheerleaders for the demolition of our federal financial aid system were “mugged by reality.” The two assumptions that served as a foundation for more than a decade of higher ed policy advocacy turned out to be wrong.

First, it turns out that when you cut back on federal financial aid, schools do not rush to lower tuition. This premise—a sort-of reverse Bennett Hypothesis—was always in tension with everything we know about higher ed economics. It turns out it was just empty rhetoric driven by right-wing think tankers with ulterior motives and center-left dupes who really wanted to dress up as serious dealmakers on The West Wing.

It was this type of empty rhetoric that actually helped to create the momentum in Congress to cut $300 billion in financial aid to give tax cuts to billionaires and big corporations in the recently passed One Big Beautiful Bill Act.

Colleges are now cutting all kinds of back-room deals to avoid doing this thing that is obviously not in their financial self-interest. Schools are even rushing to put their own money on the line to expand private student lending and maybe even align admissions decisions with lenders’ underwriting limits, as one long-time student loan industry executive told me last week.

This isn’t just idle gossip, it’s spilling out publicly in the press now too. The president of the National Council of Higher Education Resources, a trade association that represents student lenders and debt collectors, told Jillian Berman at Marketwatch that the industry is making new investments in technology to allow lenders to underwrite and manage six-figure private student loans for the first time.

“If the federal government is going to pull back, whether we like it or not, more students are going to rely on private loans,” he told Marketwatch.

We all saw this coming. The framers of the “cut financial aid and tuition falls” fantasy are now engaged in a public effort to move the goalposts—joining a chorus that includes leaders in the private student loan industry to plan for a resurgence in private student lending.

Never mind that the promise was lower tuition. Never mind that these very same private student lenders got caught cheating students a generation ago, leading policymakers to push private loans to the margins of financial aid. Never mind that, predictably, the incumbent private loan industry will not underwrite 40 percent of students with lower credit, income, and wealth. As a result, the most vulnerable students and families—who often stand to gain the most from the socioeconomic mobility once promised by college degrees—will be less likely to access a higher education.

Fun times.

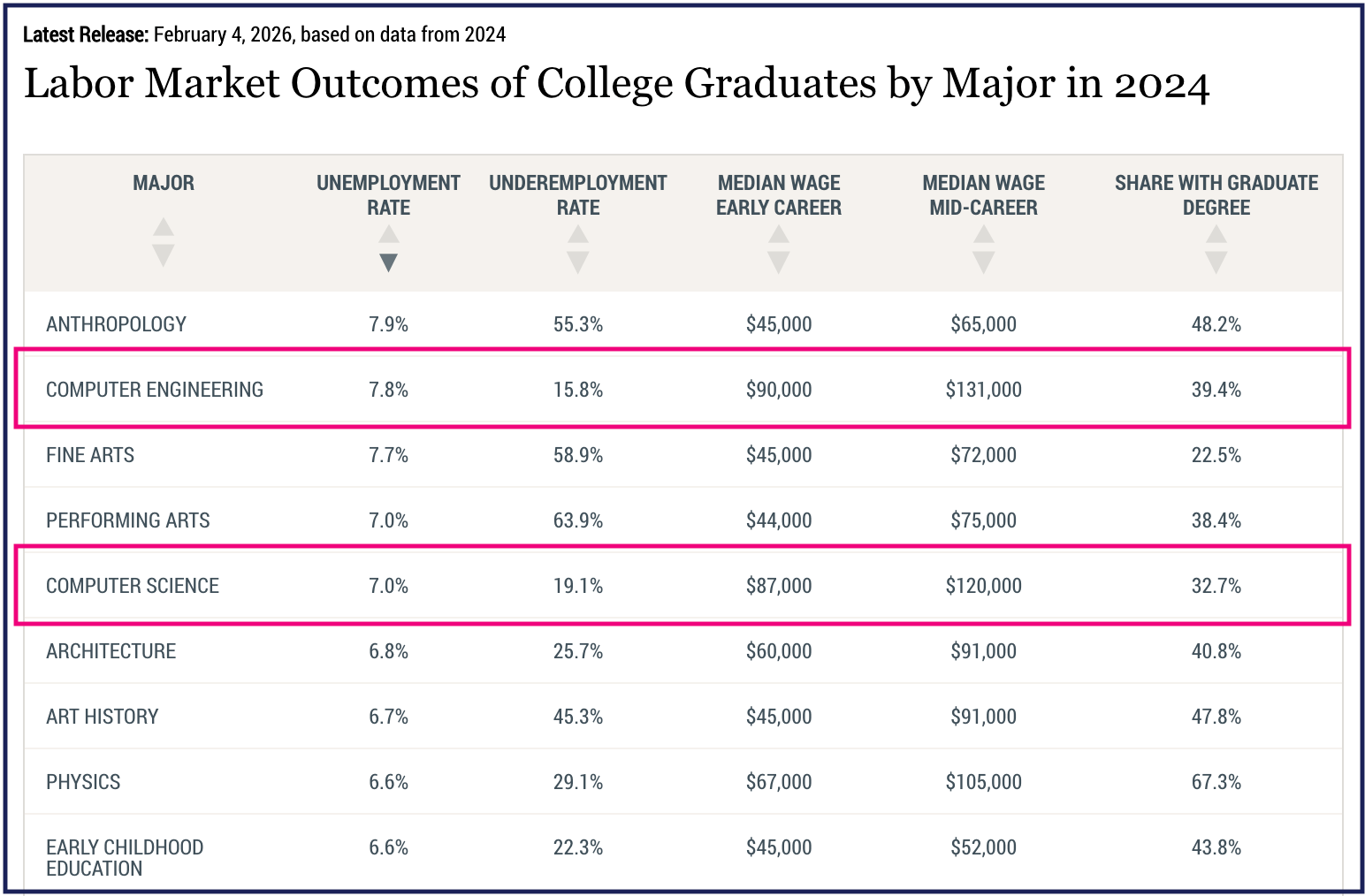

A second assumption that also appears to be catastrophically wrong: it turns out that learning to do computer stuff is not a bulletproof strategy to maximize the return on your investment in higher education. New data published by the Federal Reserve Bank of New York shows that even in a relatively strong economy with relatively low unemployment, recent grads with computer science and computer engineering degrees face levels of unemployment once reserved for art history majors.

This observation cuts against a mountain of conventional wisdom around how to plan and prepare for a career after college. Computer science and computer engineering degrees were supposed to be an economic slam dunk—the jobs of the future in a dynamic economy. President Obama famously told kids across the country that it was time to learn to code.

The central tenet of higher education policymaking by both parties for more than a decade has focused on maximizing so-called “return on investment” or “ROI” for students going into debt for a degree. The theory goes, “high ROI” majors are good stewards of federal financial aid while “low ROI” majors are not. Taken to its logical endpoint, higher ed policymakers should precisely target federal financial aid to ensure federal money flows to the programs that build the workforce of the future.

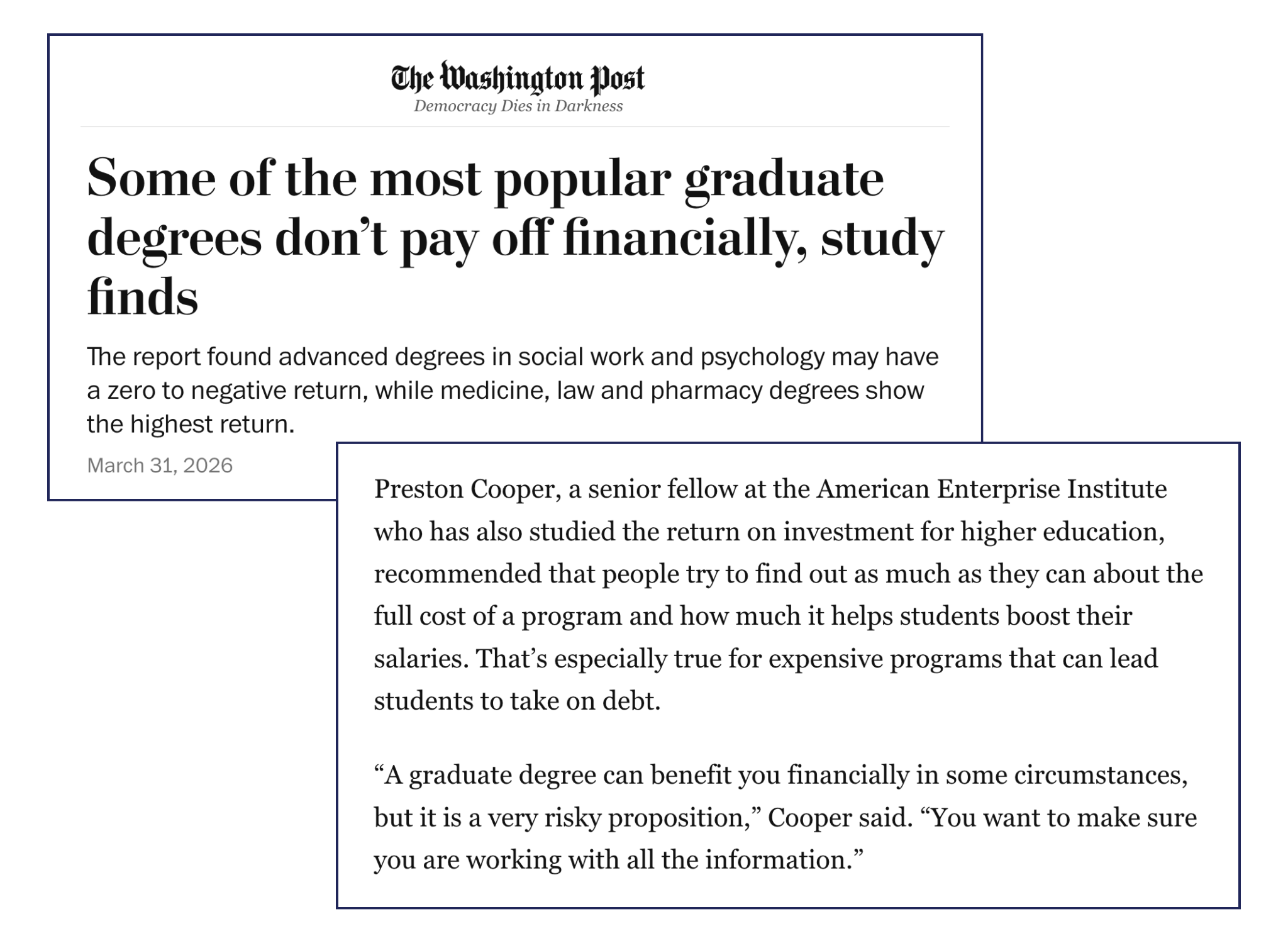

The rapid shift in job prospects for computer science grads exposes the limits of policymakers’ ability to assess the value of higher education on purely economic grounds. It also shows the tremendous hubris among the wonks who tell other people to make gigantic financial bets based on this limited information. Yet last week, these very same wonks were, once again, crowing in The Washington Post about how students could reliably use past performance to predict the future economic return of a graduate degree. Never mind the fact that there’s a four-year-or-more delay between when students would have to choose their major and perhaps begin taking prerequisite high school classes, and when they enter the job market. And never mind the obvious fact that if you steer millions of students into one field, the labor supply you create could exceed the demand and ultimately drive down the very wages and job prospects used to justify that steering. It’s especially ironic that the pro-“market” wonks in Washington have conveniently ignored this.

The reality for students and families is that wonks are lousy at predicting the future. It’s impossible to have, in the words of American Enterprise Institute’s (AEI) Preston Cooper, “all the information” when pursuing a higher education. All of the available information in 2020 would not have helped a computer science major predict a 25 percent rate of unemployment or underemployment four years later.

After a decade of the D.C. higher education establishment cooking up increasingly kooky schemes to cut back federal financial aid while preaching about using ROI to “shop” for a good deal, the rapid changes in labor market dynamics and college pricing should make us approach these proposals with a little more humility. If anything, after the One Big Beautiful Bill, we should see through these ideas as window dressing for multi-billion-dollar handouts to private student lenders.

All of this should put wind at the backs of those of us fighting for a free, universal public option for higher education. Only our government has the capacity to weather major shifts in labor market dynamics. America once used public money to help lower the financial stakes for students and families when choosing a major, a program, a degree, or a school. We need to do so again.

###

Mike Pierce is the Executive Director and co-founder of Protect Borrowers. This blog was also published on In Debt, a Protect Borrowers Substack.