BankMobile Is on the March Just as Oversight Has Disappeared

By Ben Kaufman | May 28, 2026

Come with me, if you will, to the land of the pines, where the upcoming IPO of First Carolina Bank illustrates how Trump’s attack on consumer protection is putting millions of students at risk. And not for the reasons we usually talk about. Instead, the issue here is a name that folks in the students’ space know well, and that untold numbers of students are about to learn: BankMobile.

You see, First Carolina is mostly not a particularly remarkable bank. It has $3.3 billion of assets (a lot for you or me, but not that much for a bank), the better part of which are real estate loans. It has nine locations across four states and a Twitter account that hasn’t posted since March of 2024. Its board and management appear to be resoundingly (appropriately) boring. Etc, etc.

But First Carolina is extremely remarkable because in late 2024 it paid $67 million to buy BM Technologies, aka BankMobile (pronounced like “a bank that is mobile,” not like “batmobile”). And that means First Carolina plays a massive role in the so-called “campus cards” market, one of the shadiest and most scandal-laden areas of campus finance.

Last week, First Carolina filed an S-1, the form companies submit to the U.S. Securities and Exchange Commission (SEC) ahead of going public. That S-1 shows that students are at greater risk than ever before from BankMobile given First Carolina’s plans to monetize the company. With the federal agencies that oversee the campus cards space asleep at the switch when they aren’t actively weaponizing themselves against the public, these possible harms to students couldn’t be arriving at a worst time.

We need everyone with any power to do so—from state enforcers to lawmakers, advocates, and beyond—to show up and protect students from BankMobile.

The Campus Cards Space is a Predatory Mess

To review: When students take on federal student aid (like federal loans and Pell grants), any money left over after tuition and other expenses can be sent to those students via a school-sponsored debit card linked to a bank deposit account. We call those cards “campus cards.” (This Consumer Financial Protection Bureau (CFPB) report has a good overview of the market structure.)

When I say “school sponsored,” though, I mean that the school essentially makes a back-room deal providing a bank exclusive access to its students—sometimes letting the bank operate under the school’s branding—in return for that bank managing the school’s financial aid flows. The school can also end up pocketing millions of dollars taken as a cut of the fees that banks are able to push onto students, including costly overdrafts, charges for failing to maintain minimum funds, fees for inactivity, a payment just to check your balance, and much more. Students have even faced fees when their school is already paying the card company to handle their account, making any fees duplicative. In its most recent campus banking report, the CFPB found that campus cards generated $15 million in revenue for colleges.

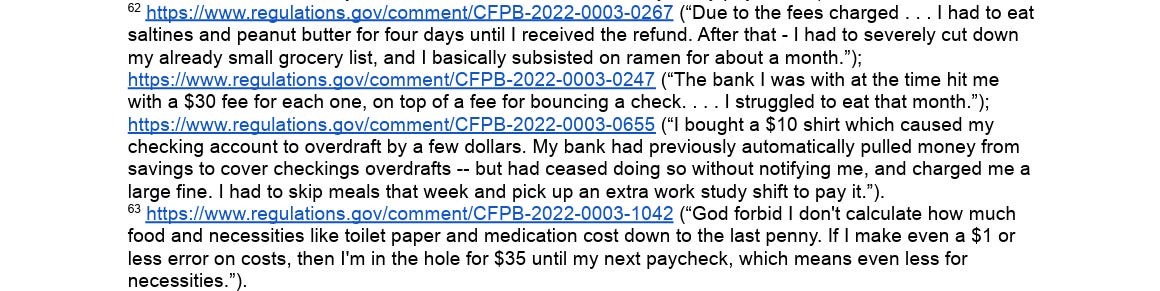

People have been working to draw attention for years to the ways in which this space is a disaster for students. In particular, folks in government agencies, on the Hill, and in the consumer advocacy world have all tried to describe how companies in the campus cards market load up their products with huge, unfairly structured fees that can cost students hundreds of dollars per year. The U.S. Department of Education (which oversees the campus cards program) made certain rules in 2015 aimed at addressing the worst tactics in the market, and the Bidens tried to expand on those safeguards, but the harm has basically continued. E.g., check out the footnotes starting on page 9 of this letter for firsthand narratives from students about how they recently had to forgo food, electricity, textbooks, and more because of junk fees on campus cards on which their schools signed off.

The CFPB also found in its 2023 campus banking report that students “at Historically Black Colleges and Universities (HBCUs), for-profit colleges, and Hispanic-servicing institutions (HSIs) all pay[] higher-than-average fees per account” on campus cards than students at other schools. Bad!

Enter BankMobile, the Shady Leader of Campus Cards

One company dominates the campus card space: BankMobile (BM). And that company already had a track record riddled with red flags before First Carolina bought it in 2024.

BM started in 2015 as an online banking division of Customers Bank, a large regional bank based in Pennsylvania. That is, BM aimed to be the “first and only bank offering a no fee, purely mobile and tablet banking platform.” (Here are some old and yes kinda impolite but nevertheless correct tweets from me about the wild nepotism that surrounds BM, like e.g. CEO succession went from the founding CEO to his daughter, and the company went public by merging with a SPAC sponsored by the then-CEO’s dad and brother.)

To help things get started, Customers Bank bought the student banking arm of a company called HigherOne, which had recently been the subject of a massive scandal alleging predatory fees and marketing targeted at students. Those issues led to a $25 million settlement between HigherOne and the Fed.

Pretty soon, things at BM got ugly. By 2017, the company’s CEO was saying it wouldn’t be able to operate profitably. In 2021, BM spun off to become its own company, but it still struggled. (They also tried to buy a bank at one point and it fell through, which is not the point at all but I think it somehow underscores how shambolic this company is and has been.)

Then, in 2022, the CFPB dropped a giant report on campus cards, and we learned that BM had basically taken over the space. That is, BM controlled nearly 70 percent of the campus cards market, boasting partnerships with “approximately 750 university partners” and handling “over $13 billion in disbursements” of financial aid. (Later, BM’s share of the market would rise to about 80 percent.) But the company appeared to be leveraging this market position at students’ expense.

In particular, it turned out that BM was allegedly deceptively directing students into more expensive deposit accounts when cheaper ones were available, incorrectly telling students they would have to wait longer for refunds if they didn’t use BM’s products, and sneakily making it so that financial aid money wouldn’t count toward students meeting BM’s minimum account balance requirement—even when the entire idea of its accounts were to be a place people could access financial aid money. Those moves allegedly helped BM extract almost $13 million from students just in fee revenue in a single year. (California’s consumer financial regulator later settled with BM in 2023 for misleading students in a variety of ways.)

First Carolina nevertheless became BM’s bank partner in 2023, and then bought it outright in 2024. (We at Protect Borrowers wrote a letter to the FDIC and NC regulators warning against allowing for the 2023 partnership, and, oops it didn’t work.)

Then, for a while, there was silence.

But Then First Carolina Filed Its S-1, Revealing Grave Consumer Risks

That is, my Google Alert for BankMobile went off, and it led me to First Carolina’s S-1. What I found in that filing made clear that students are at greater risk than ever before from BM via First Carolina’s plans to monetize the company. In particular:

- FC/BM are going to try to push additional products on students, just as oversight has receded. FC describes students as ideal depositors—it pays no money to acquire them (in fact, schools pay BM to hand them their students!), and FC does not appear to believe it has to pay much interest to keep students at the bank. As FC puts it, the BM acquisition added “$535 million in deposits with a cost of 0.02%” (read: at a low cost). In FC’s words, the addition of those accounts reflected student disbursements being an “evergreen pipeline” of business and students themselves being “a significant source of low-cost deposits” that FC can lend out at a higher rate.

But FC also makes clear that it has bigger plans for these essentially captive students, and those plans involve students taking on even more of FC’s financial products. Their S-1 says:

“As we are the platform through which students receive their disbursements, we have the unique opportunity to create durable and long-lasting relationships with high engagement with them. With minimal [acquisition cost] of student deposits accounts, converting these students to long-term, everyday banking customers is a key objective in expanding our deposit base.”

That could be fine—it could just mean that FC will woo students by presenting them wonderful banking offerings that they just can’t resist.

But it could also mean making a buck by steering students toward stuff they don’t want, need, or fully understand, including through deception—just as BM was already alleged to be doing in the CFPB report I mentioned above. If so, those risks will arise at a time when the U.S. Department of Education and the CFPB are both somewhere between asleep at the switch and actively weaponizing themselves against protecting the public. The unfortunate result is that we will likely learn of any abuses only long after they have bubbled to the surface, and even then, it isn’t obvious that any of the folks meant to supervise this space will deliver redress.

- The fees students face to use their own money could be about to balloon. BM’s student accounts continue to have a variety of dubious fees including a $2.99 monthly service charge. The S-1 offers us new visibility into how much of a cash cow these fees remain for BM, amounting to almost $2 million in the first three months of 2026 alone:

This figure is particularly notable given that the BM segment nevertheless operated at a $909,000 loss overall in the first three months of 2025, as fees are one of the three “primary ways” that FC describes itself as making money on student accounts. (The other two are the fees it charges universities and the money it makes lending out students’ “lost-cost” deposits.) Putting the pieces together, there appears to be a very real risk that FC might aim to close the hole in the BM segment’s profits by laying new fees on students or increasing existing ones. As above, if it does, the folks who would be keeping an eye out will be nowhere to be found.

- Students’ data could be at risk, and FC/BM is already using it for surveillance-based targeting. The S-1 says (emphasis added):

“We possess data at both the account level and the transaction/instrument level (merchant name, location, merchant category code, dollar value, etc.) with over seven years of history. Leveraging this information, we are deploying scalable, data-driven marketing initiatives based upon proven methodologies of automated portfolio screening, advanced diagnostic evaluations, defined outcome protocols, and applied treatments.

“For example, we are targeting other cohorts of likely graduates with incentives to make our BankMobile Platform their choice for payroll direct deposit.”

And, worse:

“Additionally, we believe there will be strong revenue growth capabilities through . . . our Payments business and BankMobile Platform businesses as well as incremental fee income growth identified through our data analytics platform via interchange income, account fees and payments.”

That is, FC/BM says that it believes it can cash in by using students’ transaction data to target fees at them. All under the noses of both schools and regulators!!!

If BM does take actions that harm students, those injuries will immediately involve massive scale. In particular, the S-1 indicates that BM now moves “$13.5 billion annually to 3.2 million student[s]” on behalf of 750 schools across America. BM is also growing at a breakneck pace: the S-1 reported that the company added 148,000 new accounts in 2025 alone, meaning it may have increased accounts 20 percent from the 727,060 total accounts the CFPB tallied in 2024.

Plus, if any of these risks materialize, BM brags in the S-1 that universities would still be likely to partner with them. Schools, it says, “are reluctant to leave” its network, because “switching costs are comparatively high.” That is, even as it burrows deeper into the campus cards market, FC/BM does not appear to think that either students or universities are particularly savvy or runnable customers.

Everyone With Any Power to Do So Has to Step Up to Protect Students

We talk a lot about how dangerous of a moment this is for consumers with “the lights out at the CFPB and state AGs already stretched thin.” Things like the FC S-1 illustrate what that risk really looks like. A bank got into the campus cards business, a space where even small harms can balloon into personal financial crises for students. That bank did so by buying a company with a track record of questionable consumer-facing conduct, and it now reasonably intends to make a return on that investment. Students have already been hurt by BM, and all signs point to heightened risks.

In this moment, we need real supervision and oversight to make sure that return doesn’t come at students’ expense. That means everyone with any amount of authority has to step in to protect students from BM.

###

Ben Kaufman is a Senior Fellow at Protect Borrowers. He writes a weekly column for In Debt, a Protect Borrowers Substack, called “This Week In Debt.” Ben previously worked at the Consumer Financial Protection Bureau. This blog was also published on In Debt.