The Case for a Buy Now, Pay Later Bill of Rights

By Mike Pierce | April16, 2026

Americans are being squeezed by high prices. Families are being targeted with offers for risky new kinds of debt. A growing share of borrowers are falling behind on these loan bills, even as lenders’ profits soar. Something needs to change.

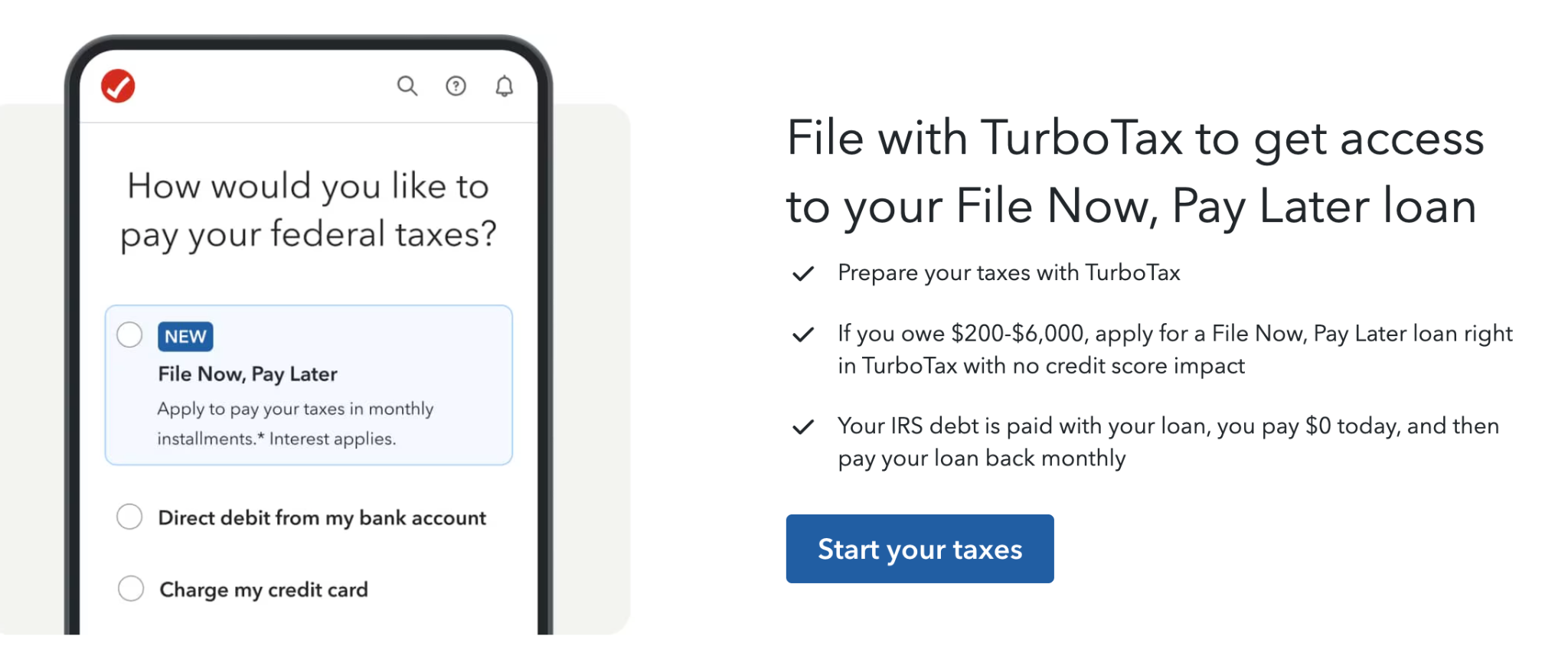

This week, millions of Americans who used TurboTax to file their tax returns were presented with an offer to finance any tax bills owed to the IRS using a financial product called “File Now, Pay Later.” File Now, Pay Later loans can be short and cheap or long and expensive. The TurboTax fine print promises rates between 15 percent and 33 percent—as high or higher than most credit cards. Functionally, this is just closed-end installment lending, but offered by the tax prep giant that charges you to do a thing that should be—and briefly was—free.

TurboTax only exists because of a policy failure that looks a lot like corruption. Now its owner Intuit is using its dominant market position to push people into risky, high-rate debt. This is a perfect illustration of why Americans hate Trump’s broken economy.

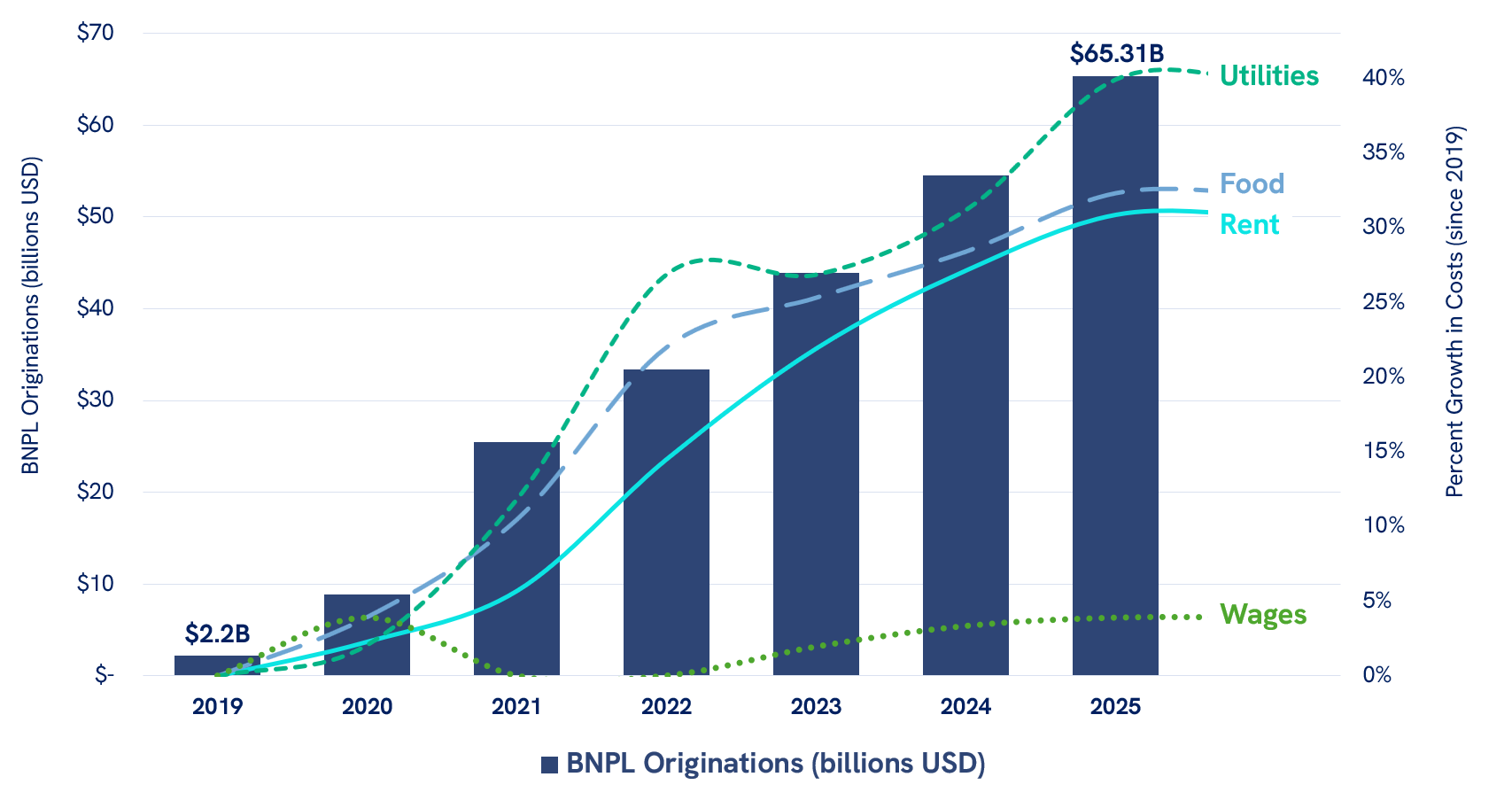

As rising costs continue to strain families’ finances across the economy, nearly half of all Americans have taken out a short-term loan to pay for a routine expense, according to the most recent edition of a benchmark survey published by the fintech company Lending Tree. These short term loans, marketed as Buy Now, Pay Later products (BNPL), can carry a ton of junk fees, require people to waive their rights, and may just be a vehicle for lenders to gobble up information about you to package and sell to other companies.

The companies that make these loans cut deals with merchants across the economy to target families with credit offers intended to exploit their desperation to make ends meet. It’s not just at tax time. Americans are going into debt at the grocery checkout aisle, when their rent is due, in the doctor’s office, at the vet, when the time comes to pay the electric bill, and beyond.

Lending Tree’s survey also shows a spike in Americans who report missing payments on these loans—part of a surge in borrowers falling behind on their credit cards, student loans, and auto loans. Nearly half of all Americans who used a BNPL loan report that they missed at least one payment over the past year—“up from 41% in 2025 and 34% in 2024.”

You might think that a surge in borrowers missing payments would expose some underlying weakness in the economics of BNPL. For many BNPL lenders, the opposite is true—when borrowers miss a payment, they may be hit with enormous penalties and fees. Not all BNPL lenders charge late fees, but some charge fees as high as 25 percent of the missed payment, turning a product marketed as “free” into a debt trap. And unlike credit cards which come due at the end of each month for all the purchases made over that time period, BNPL lenders issue individual loans for every transaction a borrower makes, meaning that one missed paycheck or lapse in funds can lead to a cascade of late fees across a dozen or more debts.

This helps explain why the biggest companies in this market are raking in record profits.

Where does that leave the nearly half of Americans who use BNPL?

Families struggling to keep up with rising costs resort to debt because it is often the least-bad choice in a set of terrible options. In 2025, New York passed a new law that tips the balance of power back towards families and reins in some of the worst practices by the fintech companies making these loans. Earlier this year, New York’s Department of Financial Services (NYDFS) proposed new rules building on this foundation and expanding protections for families.

Former Consumer Financial Protection Bureau (CFPB) Director Rohit Chopra put together this explainer earlier this week, putting into plain language the state of play for families who go into debt to stay afloat. He ends his pitch with a simple idea: we need a Buy Now Pay Later Borrower Bill of Rights.

Chopra has it right. Families turn to debt in moments of desperation, often as a last resort—borrowing for medical costs, financing their rent, going into debt to heat their homes. At the same time, the American economy is struggling with rising healthcare, housing, and energy costs. When companies can push debt onto customers who cannot afford their bills, it drives up costs for all of us.

Policymakers can go even further than the guardrails proposed in New York, and there is a role to play for cities, states, and the federal government. As the BNPL industry continues to grow, policymakers need to step in now, before it is too late.

We’ve put together an outline for a new Buy Now Pay Later Borrower Bill of Rights, which builds upon the framework passed in New York. We also include some of the common sense reforms put in place in the housing, credit card, and student loan markets over the past two decades and address the unique risks posed to families who use BNPL products.

To protect borrowers, policymakers should:

- Make sure “free” actually means free. Many companies in the BNPL market use subscription charges, transaction fees, and other junk fees to mask the true cost of the credit they are extending to their customers. If a BNPL lender markets a loan as “free” or “0% interest,” it should actually be free.

- Ban usury. If we wouldn’t let a loan shark charge sky-high interest rates, we shouldn’t let a tech company.

- Ban voluntary “tips.” Your lender is not your bartender. Financial companies should offer clear, up-front pricing with no hidden fees. BNPL lenders should never solicit tips or other voluntary payments from borrowers; borrowers should only pay for the financial products or services provided.

- Ban chatbot doom loops and dead ends. Everyone should have a right to speak to a real person and get a response to basic questions and complaints. Where companies rely on AI chatbots to provide front-line customer service with limited functionality, they must also provide one-button access to a customer service rep who can process complaints and handle higher-level customer service functions. If a borrower runs into trouble, a company should not be able to charge late fees or damage the borrower’s credit until their complaint is resolved.

- Guarantee the right to a full refund. Unlike credit cards, individual BNPL loans are typically tied to the purchase of a single item, a basket of goods, or a set of services. BNPL borrowers typically have the option to return purchases or seek a refund for services by working directly with a merchant. When a borrower unwinds a purchase, BNPL lenders should provide an equivalent process to unwind an accompanying BNPL loan, working with merchants to resolve returns with no additional costs, fees, or charges, to borrowers.

- Ban the sale of borrowers’ data and protect borrowers’ privacy. NYDFS proposes strong guardrails to protect borrowers’ privacy, only allowing lenders to share data with third parties where “reasonably necessary to provide the consumer’s requested product or service.” Lenders should never sell their customers’ data and never use private information to cross-sell other financial products.

- Ban predatory lending. BNPL lenders should underwrite loans based only on risk— ensuring borrowers can repay the debts they borrow, but not pricing loans or extending credit to maximize borrowers’ indebtedness or costs. Because these firms often rely on AI models that look beyond borrowers’ credit profile and income, BNPL lenders should also ensure any data collected or used for marketing, pricing, underwriting, or other functions is necessary to assess risk and price based on risk.

- Cap late fees at $8. BNPL lenders are not alone in squeezing high late fees out of struggling borrowers. NYDFS restricts high late fees and assumes an $8 late fee is acceptable, mirroring the framework the CFPB once proposed for the credit card industry. We think policymakers should go further, instituting a hard $8 cap on BNPL late or penalty fees under all circumstances.

- Bring BNPL lending out of the shadows. BNPL companies should obtain a special license to make these loans and be subject to oversight by financial regulators.

- Guarantee borrowers a place to turn for help. Lawmakers should establish a dedicated BNPL borrower advocate to help families handle problems that emerge when things don’t go according to plan. Modeled on the state-level and federal “student loan ombudsman” offices created to address the student debt crisis, these government officials can help resolve complaints and drive oversight by financial regulators.

- Let borrowers enforce their own rights. Every borrower should be able to hold financial companies directly accountable for following the law and respecting their rights, including BNPL lenders, their bank partners, and any other service providers. A state or local BNPL Borrower Bill of Rights should come with a private right of action, including the right for borrowers to obtain attorneys’ fees in court and the right to additional damages if a company willfully or knowingly breaks the law. A federal BNPL Borrower Bill of Rights should also ban forced arbitration and class action waivers in BNPL loan contracts.

In 2026, everything is also a story about AI.

Across the financial sector, companies are scaling up their investments in AI and machine learning. Lawmakers and the courts are playing catch-up as the framers of the AI boom seek to shirk liability under a range of laws that apply to private firms across commerce.

In this context, it’s helpful to revisit the state of the law today, as we see it. Where BNPL lenders use artificial intelligence or machine learning to collect and analyze borrowers’ data, compile and maintain customer profiles, target marketing materials, or perform other services, BNPL lenders are liable for the conduct of these models or agents. Where BNPL lenders use artificial intelligence or machine learning to make decisions about credit offers or loan terms, federal fair lending and credit reporting laws require that these firms notify borrowers of any adverse action, clearly explain the basis for this action, and offer borrowers the opportunity to submit a complaint challenging the action. Where a BNPL lender purchases or licenses a model or agent from a third party to perform these functions, both parties are jointly and severally liable for any injury caused to a borrower.

This is table stakes. As lawmakers consider various legislative proposals at every level of government to “regulate” AI, these first principles must hold fast. Congress and federal financial regulators should also consider the factors that AI models consider when underwriting and pricing consumer credit—pushing the industry away from exotic and overly complex models towards factors proven to correlate with risk: how much money borrowers make, how much cash they have on hand, and their track record repaying other debts. Where lenders deviate from considering these factors, they should be prepared to prove to regulators and borrowers why additional information is needed to assess risk—and they should never use this information to cross-sell other products, collect other debts, or allow their merchant partners to engage in surveillance pricing.

These guardrails build on existing state and federal bans on unfair, deceptive, and abusive acts and practices, bans on false advertising, and privacy laws that already fence in some of the worst conduct by financial companies, including BNPL lenders. While we wait for lawmakers to put in place a new BNPL Borrower Bill of Rights, enforcement officials at every level of government should vigorously enforce the laws on the books.

Borrowers and honest businesses always benefit when borrowers’ rights are clear and enforceable. It’s time for a BNPL Borrower Bill of Rights.

###

Mike Pierce is the Executive Director of Protect Borrowers. This blog was also published on In Debt, a Protect Borrowers Substack.