A Closer Look at Our Broken Judiciary, Student Debt Relief, and the Politics of Affordability in 2026

By Mike Pierce | March 3, 2026

UPDATE: Since publication, a group of right-wing AGs continues to pursue a court order suspending the SAVE plan again. As of March 5, no court has stepped in, and SAVE is still alive. However, we have seen no action from ED to implement the program. Members of Congress are calling on ED to give borrowers their legal rights. Borrowers should stay tuned. In the meantime, borrowers can reach out to their Congressional offices if they’re experiencing issues with their student loans.

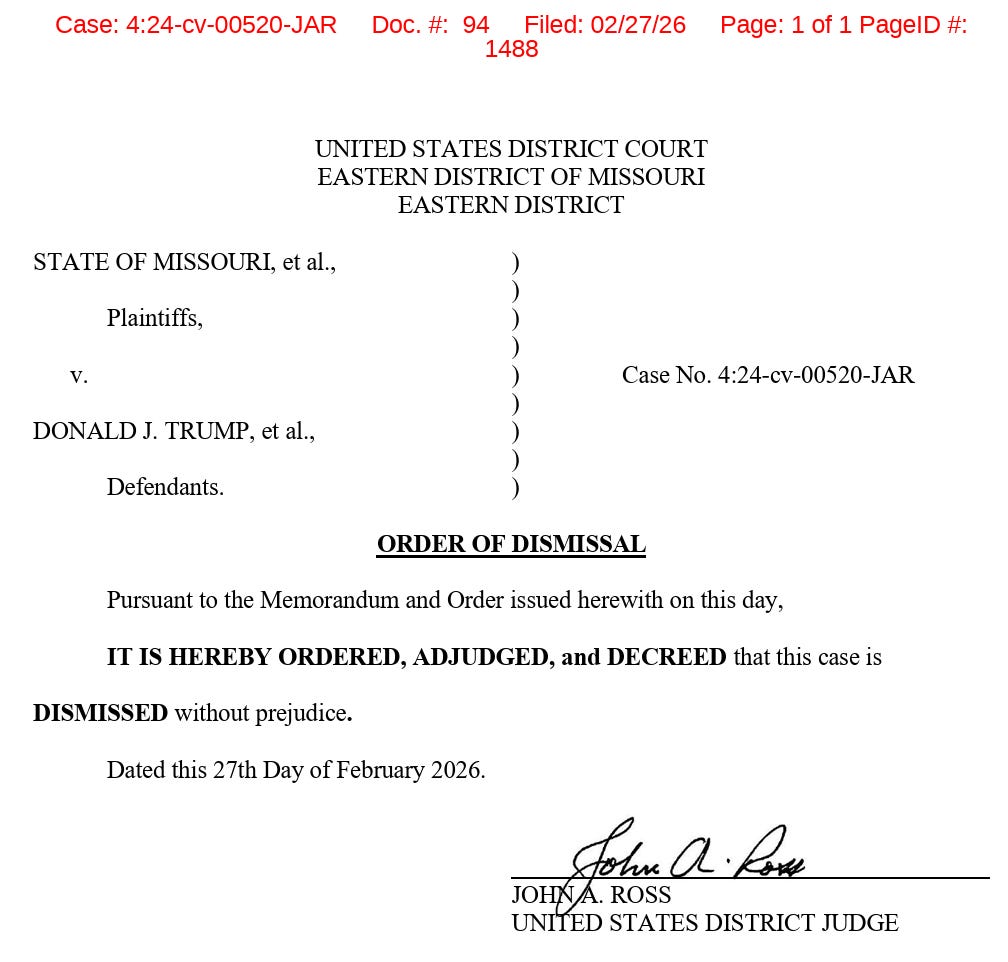

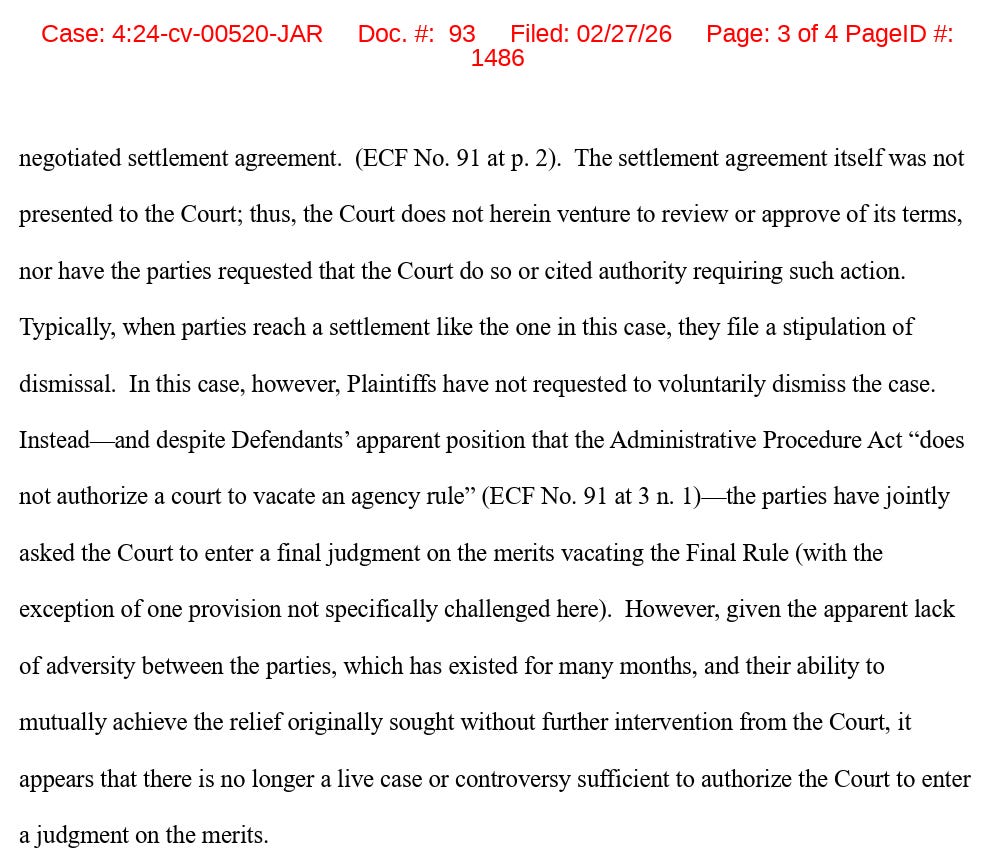

On February 27, a federal district court judge in Missouri handed down an extraordinary order, dismissing a lawsuit by a group of right-wing attorneys general seeking to kill a Biden-era student loan repayment plan, known as the Saving on a Valuable Education (SAVE) plan. SAVE promised lower monthly payments to millions of borrowers and offered a path to debt cancellation for millions more over time. Even today, there are likely tens of thousands of people who already have a right to have their debts canceled immediately, should ED allow this plan to go into effect as the court designated.

This court order reopens the window to cancel student debt, at least for now.

There is a unified theory of what the hell is happening here.

Republicans across the country campaigned against this student debt relief and Trump’s Education Secretary proudly crowed in the Wall Street Journal op-ed page that the era of loan forgiveness was over. Fortunately for borrowers, reports of SAVE’s legal demise appear to be greatly exaggerated.

To understand what happened, you need to understand that, fundamentally, right-wing politicians are cowards who lack the confidence of their convictions—except for their conviction to cut taxes for billionaires and big corporations.

If Trump’s Education Department wanted to roll back SAVE and jack up costs for millions, they could have rewritten the SAVE rule on day one. But then President Trump would have been the cause of a policy shift that would have immediately increased the cost of repaying a student loan by more than $3,000 per year for a typical family. Nearly 8 million people would have seen their costs climb, even as voters across party lines beg Trump to do something about America’s affordability crisis. Ending SAVE is terrible politics.

Immediate action to rewrite these rules would also have denied Congressional Republicans a key budget gimmick they could use to ‘pay for’ tax cuts for billionaires and big corporations—again, Republicans’ only actual, core belief. As it stood when Trump came into office, Congressional budget scorekeepers estimated that legislation to repeal SAVE would “save” the government more than $130 billion.

So Trump’s Education Department officials and Republican lawmakers cooked up a different scheme—one that would capture billions of dollars of budget “savings” but delay the economic pain to borrowers until 2028, all while letting right-wing AGs and a federal judge be “responsible” for killing off this payment plan.

The first step in this scheme went off without a hitch. The so-called One Big Beautiful Bill Act (OBBBA) eliminated the statutory basis for the SAVE plan—a piece of the Higher Education Act that had been the basis for a series of Income-Driven Repayment options for nearly three decades. To insulate themselves against the blowback from this radical policy shift, lawmakers delayed the effective date of this change until 2028 (see, cowards).

At the time, this had no practical effect because of the shenanigans still playing out in a federal courthouse in Missouri. Back in 2024, a coalition of right-wing AGs won a court order temporarily blocking SAVE from going into effect—an order that was expanded by the arch-conservative 8th Circuit Court of Appeals and is a cause of the deeply dysfunctional status quo in the student loan system.

On February 27, the court order blocking borrowers’ access to SAVE died.

The federal district court judge overseeing this lawsuit dismissed the right-wing AGs’ challenge—holding that because of the obvious and explicit coordination between the AGs and Trump’s Justice Department, there was no “live case or controversy” and the court lacked jurisdiction to invalidate the SAVE plan.

In effect, this whole scheme seems to have collapsed under its own weight. Now borrowers may get some relief.

[ed. note: there is a related, separate case in a Kansas federal court where a different, competing coalition of right-wing state AGs sought similar relief. Because these cases covered the same claims, the Kansas court held back in deference to the Missouri court. This case remains on file, but there is no injunction in place, so its existence has no immediate effect on borrowers’ rights.]

What happens next is not really up to Linda McMahon.

As of February 27, 2026, borrowers’ rights are restored. There is no court order blocking SAVE, no new federal rulemaking rescinding these rights, and OBBBA only sunsets the underlying statute in 2028. Any borrower who has met the criteria for debt cancellation under SAVE has an entitlement to this debt relief, effective immediately.

Of course, Trump’s billionaire donor-turned Education Secretary will hem and haw about her duty to follow the law and cancel these debts, but the law is clear. Expect a slew of lawsuits from borrowers if the debt cancellation machine doesn’t kick back into high gear.

The biggest open question in my mind is how forcefully and how publicly the Trump White House wants to be seen blocking these borrowers’ rights—particularly now that it no longer has right-wing AGs and federal courts to blame.

Could the politics of the affordability crisis turn Trump into a debt cancellation evangelist in 2026? Stranger things have happened.

###

Mike Pierce is Executive Director of Protect Borrowers. This blog was also published on In Debt, a Protect Borrowers Substack.