A Pair of Polls—One Old, One New—Bring America’s Affordability Crisis Into Sharper Focus

By Mike Pierce and Emily DiVito | March 5, 2026

Late last year, Groundwork Collaborative and Protect Borrowers published the results of a deep dive into Americans’ debts conducted by Data for Progress, looking closely for the first time at a broad range of routine living expenses now financed by Buy Now, Pay Later loans. Yesterday, we published a new poll, asking a similar set of questions about the credit card debts owed by people who cannot pay off a credit card bill each month. In both cases, people are going into debt to pay for the basics—from groceries to medical care to household goods.

These two polls speak directly to each other and tell a clear story about rising costs and families’ use of debt to stay afloat. The upshot: Everywhere you look across Donald Trump’s economy, debt is masking a fundamental weakness in families’ finances.

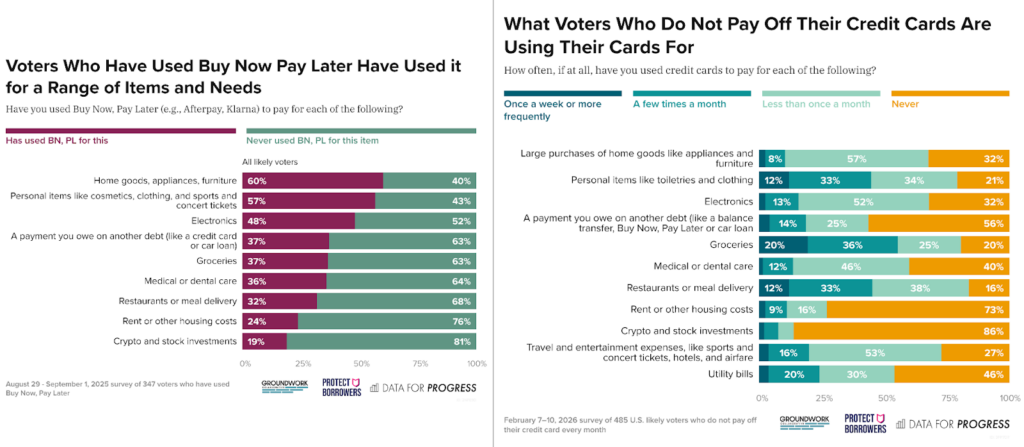

Look at these two charts:

Two Polls, One Story: Debt is Keeping Families Afloat

Americans are in debt to pay for basics like rent and groceries. Debt also heats our homes and pays for kids’ doctors’ visits. This helps explain why everyone is angry about Trump’s economy, even with relatively low unemployment and consistent economic growth. Families feel squeezed in a way that extends far beyond the size of their paychecks—the product of a vice grip of rising costs and the cost of credit.

When you talk to working class and middle class Americans, they are quick to tell you this directly. Last month, Protect Borrowers released a survey we conducted with our friends at AFT, asking more than 7,500 teachers, healthcare workers, and other AFT members to describe their financial circumstances in their own words.

Brittany, an AFT member from New York, put it better than we ever could. She told us “[c]hild care costs have put a significant strain on our family’s finances. Up until this past year, I’d never carried any debt (with the exception of my home/auto loans). I am now in nearly $20,000 worth of credit card debt due to low pay (despite working two jobs) and the astronomical cost of child care and daily essentials.”

Matt, an AFT member from Texas, described how rising energy costs pushed his already brittle financial situation past the breaking point. Matt said “[f]or the first time we had our electricity cut off at our house in [December]. … [I] have been teaching since 2007 but with debt from my child’s (special needs) medical [debt] & high energy costs we had to be late on energy bills then we got really behind and power was disconnected before Christmas.”

Ashlei, an AFT member from California, connected rising costs and unaffordable debt to her broader frustration with the economy. Ashlei told us “I’ve considered moving but my credit score isn’t good enough to get approved anywhere. My rent alone is $2,800 which is cheap compared to what I’ve seen. Trying to pay off my student loan debt is a nightmare because I can barely afford housing bills.”

These are people with good jobs and benefits—workers who a generation ago (or even a decade ago) would have been firmly in the American middle class. Today, they are crushed under the weight of everyday costs that just keep getting more expensive. They may still be drawing a middle class paycheck, but they don’t feel stable and certainly aren’t content.

Coming Back to the Politics of Debt

On Tuesday, voters cast ballots in primary elections across the country, including in hotly contested primaries in the Texas U.S. Senate race. The candidate who came out on top put cost of living front and center on the campaign trail, linking families’ rising debts, the affordability crisis, and his own personal experience.

As James Talarico explained on the stump: “Do you struggle to afford the high price of everything? So do I. Do you know what it means to carry the weight of student debt, credit card debt, and medical debt? So do I.”

Expect more of this between now and November in races across the country. Recognizing Americans’ struggles with debt is the through line between President Trump’s failure to keep his promises on the economy and what voters expect politicians of both parties to do about it.

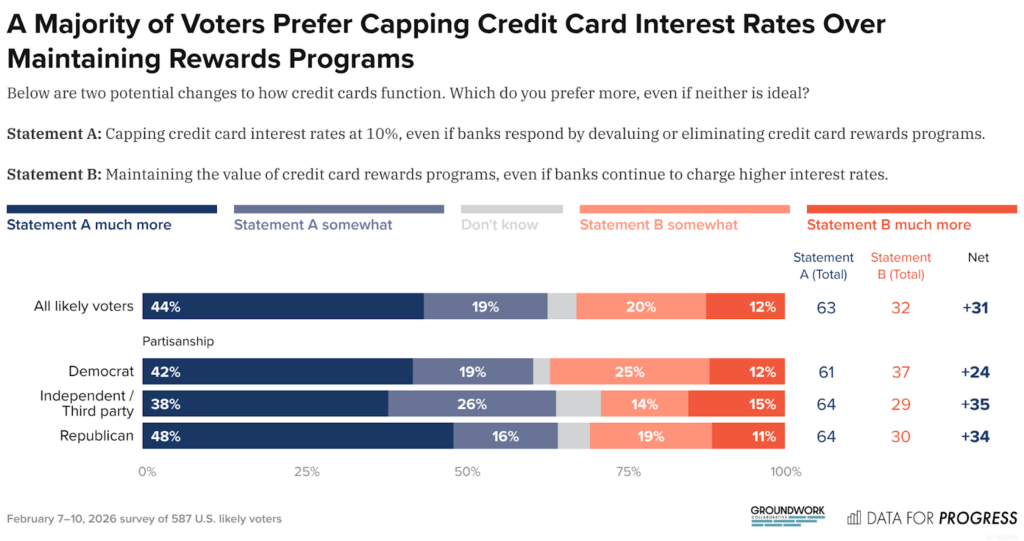

Today’s Groundwork-Protect Borrowers’ Poll makes this clear. By a 2:1 margin, Americans want lawmakers to cap credit card interest rates—supermajority support that holds even when voters are presented with credit card lobbyists’ arguments about the supposed consequences of a rate cap. This is just one policy, but it tells a much bigger story—the politics of debt will shape the way voters respond to politicians and policymakers in November and beyond.

###

Mike Pierce is the Executive Director and co-founder of Protect Borrowers. Emily DiVito is Senior Advisor for Economic Policy at Groundwork Collaborative. This blog was also published on In Debt, a Protect Borrowers Substack.