New Analysis Shows Millions of Americans, Including a Disproportionate Share of Trump Voters, Will Miss Out on Debt Relief if Trump Trades Rate Caps for Bankers’ Empty Promises

By Protect Borrowers | January 20, 2026

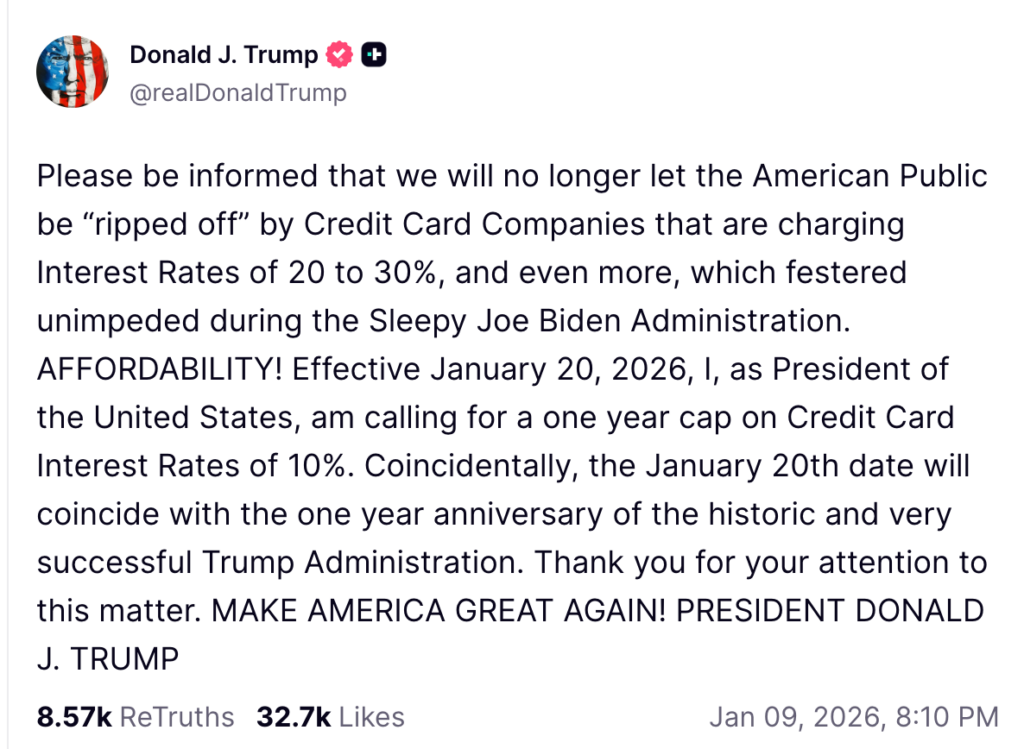

“Effective January 20, 2026, I, as President of the United States, am calling for a one year cap on Credit Card Interest Rates of 10%.” – President Donald J. Trump, January 9, 2026

“Our expectation is that it won’t necessarily require legislation, because there will be really great new ‘Trump cards’ presented for folks that are voluntarily provided by the banks.” – Kevin Hassett, January 16, 2026

Today is January 20th, and credit card rates remain sky-high.

It wasn’t supposed to be this way, at least according to President Trump. One of his signature promises on the campaign trail was a 10 percent credit card interest rate cap—an appeal to address rising affordability concerns across the nation. But over his first year in office, the Trump Administration has only fanned the flames of America’s affordability crisis.

In a whiplash-inducing moment two weeks ago, President Trump finally remembered his promise and announced that he’s calling for a 10 percent cap on credit card interest rates for one year, effective today—January 20th, 2026. That obviously hasn’t happened, despite the chaos of the last two weeks.

On January 9th, the President called Senator Roger Marshall and told him to file a rate cap bill—despite the existence of bipartisan, bicameral rate cap legislation in both chambers, sponsored by Senators Bernie Sanders and Josh Hawley and Representatives Alexandria Ocasio-Cortez and Anna Paulina Luna. He then told reporters aboard Air Force One that he expects the credit card industry to get in line (threatening “very severe things”), prompting a frantic guessing game among the press and pundits about whether there was some kind of executive order in the works.

On January 12th, he called Senator Elizabeth Warren to discuss the rate cap and other ways to address the affordability crisis. On the 13th, he endorsed legislation that purports to increase competition in card networks and lower swipe fees (… notwithstanding that his Administration approved a mega-merger that will make Capital One and Discover the largest subprime credit card issuer in the world).

On Friday the 16th, White House economic advisor Kevin Hassett appeared on Fox News to float yet another idea: banks could voluntarily offer “Trump Cards”—a credit card with a 10 percent rate that, presumably, could be underwritten and priced based on Americans’ creditworthiness. This pivot to a voluntary “Trump Card” is a credit card banker’s dream come true—no need to deliver relief to people who struggle and no government mandate to tamp down runaway bank profits.

What’s still missing, as of today (President Trump’s self-imposed deadline), is the President’s formal endorsement of bipartisan and bicameral legislation to cap credit card interest rates precisely at 10 percent, any reversal on his Administration’s move to eliminate a rule that would cap credit card late fees at $8, and any indication that Americans’ interest rates have actually gone down.

Trump campaigned as a populist, but governs as a banker.

So far, his Administration’s actions have done anything but lower costs for working families or hold Wall Street accountable.

- The Trump Administration overturned a Consumer Financial Protection Bureau (CFPB) rule that would have capped credit card late fees at $8, and dropped dozens of enforcement actions against big banks that would have returned billions of dollars to Americans’ pockets.

- They gutted staffing at the CFPB, illegally firing hundreds of federal workers who supervise and enforce the laws against big banks, and slashed the agency’s future funding by almost half.

- In his signature “One Big Beautiful Bill,” Trump and his allies in Congress made devastating cuts to Medicaid, SNAP, and student loans—programs that families rely upon to survive and help pay for college—in order to deliver trillions of dollars in tax cuts for billionaires and large corporations. There is a direct line between cuts to safety net programs and increases in household debt, including credit card debt.

- As a result of Congress’s failure to extend Affordable Care Act (ACA) subsidies, annual health insurance premiums are projected to rise by $1,016 on average this year, while food banks are running out of groceries as lines grow longer, college is becoming increasingly unaffordable for anyone without intergenerational wealth, families are taking out Buy Now, Pay Later loans to cover rent, and Americans are drowning in more debt than ever—all on his watch.

In short, though President Trump promised a rate cap during his campaign, surfacing the idea now is a massive departure from the financial havoc his Administration wrought on working families over the last year. Trump’s allies in Congress and on Wall Street also seemed shaken by this 180-degree turn, as they try to discredit the rate cap, reiterate industry talking points, and deal with tumbling bank stocks.

The Administration’s eleventh-hour pivot to “Trump Cards” only lends credence to two longstanding principles—first, the Trump Administration remains captured by Wall Street and the CEOs’ pressure game worked; and second, TACO (Trump Always Chickens Out).

But let’s cut to the chase. Trump and his allies hold the White House, Senate, and House of Representatives. As shown by their ability to pass the massively unpopular “One Big Beautiful Bill,” what he says, goes.

If President Trump is serious about lowering costs for working families, he could push his allies to pass existing legislation to cap credit card rates and sign it into law immediately.

A rate cap would provide much-needed relief to working families, and be welcomed by Americans across political and geographic divides. Consider the following:

- According to a poll conducted shortly before Christmas, over 6 in 10 Americans said the economy is not working well for them.

- Over 1 in 3 Trump voters said the cost of living is the worst they can “ever remember it being.”

- American families are now drowning in more credit card debt than at any point in history, while banks are araking in record profits.

- Half of credit cardholders have a revolving balance, forcing them to pay interest and late fees. And banks are raking in more revenue from interest and fees than at any point on record.

- As of the third quarter of 2025, 12.4 percent of Americans’ credit card balances were over 90 days past due. That’s a higher delinquency rate than at any point since 2011, or roughly the peak of the Great Recession.

- Our polling, published with our friends at Groundwork Collaborative and Data for Progress in late 2025, showed that over 8 in 10 Americans (82 percent) and almost the same share of Republicans (79 percent) support capping credit card interest rates. That makes rate caps “more popular than Santa Claus.”

New analysis: Americans need an interest rate cap, including a disproportionate share of Trump voters.

Diving deeper into these national trends, we have a new analysis showing that the very Americans who voted to put President Trump in office are especially in need of relief from sky-high credit card interest rates and late fees. In fact, credit card delinquency rates during the first few months of the Trump Administration were highest in the states that he won during the 2024 election.

Focusing on the share of Americans behind on credit card debt makes sense when we are considering both a cap on interest rates and late fees. These borrowers are hit by both charges because their debts are past due, costs that stack on top of the increasingly unaffordable markers of a stable financial life—groceries, housing, healthcare, childcare, and college.

Also view this map at: https://datawrapper.dwcdn.net/22elR/1/

Leveraging recent data covering the first half of 2025, we found that:

- The average credit card delinquency rate in states that Trump won is 4.7 percentage points higher than in other states.

- Specifically, the average credit card delinquency rate in states that Trump won is 21.9 percent, versus 17.2 percent in other states, by outstanding balance in the second quarter of 2025. (This measure equals the outstanding dollar volume on accounts that are 30 days past-due, divided by the total outstanding dollar volume of credit card balances, per state).

- The states with the highest delinquency rates are among the states that Trump won by the widest margins:

- In first place, Mississippi (which Trump won with 60.89 percent of the popular vote) has a delinquency rate of 36.69 percent;

- In second place, Louisiana (which Trump won with 60.22 percent) has a delinquency rate of 32.11 percent;

- In third place, Alabama (which Trump won with 64.57 percent) has a delinquency rate of 30.52 percent;

- In fourth place, Arkansas (which Trump won with 64.2 percent) has a delinquency rate of 28.11 percent;

- In fifth place, South Carolina (which Trump won with 58.23 percent) has a delinquency rate of 25.49 percent … and so on.

- To drive the point home (and address any skeptics perhaps wanting a more rigorous, statistical analysis): the more a state’s voters turned out for Trump, the higher its credit card delinquency rate is on average. The two factors are moderately positively correlated with a coefficient of 0.519; see below.

Also view this chart at: https://datawrapper.dwcdn.net/nzkQV/5/

All of this means that Americans who voted for Trump are disproportionately more exposed to credit card interest rates and late fees. It also means that any so-called effort to encourage credit card banks to offer voluntary “Trump Cards” would almost certainly shut out these same borrowers—people with damaged credit who couldn’t meet these banks’ existing underwriting standards.

As families deal with the real, snowballing consequences of not being able to get by—skipping meals, forgoing medical treatment, emptying bank accounts, selling their belongings, and worse—bank CEOs are raking in record profits.

According to the CFPB, in 2024, the APRs on credit cards reached their highest levels (an average of 27.5 percent) since at least 2015. Roughly half of cardholders revolved balances, paying $160 billion in interest charges and $31.3 billion in fees.

While interest drives the lion’s share of banks’ card revenues, late fees play an important role—one significant enough that bank lobbyists spared no expense to block the CFPB rule capping them at $8. To that end, capping late fees must be a core part of any proposal to provide credit card debt relief for American families. The average credit card late fee is roughly $32 per missed payment, which can present a substantial hurdle to families trying to get by. It also distorts families’ finances, as the same $32 flat fee is charged whether they are $5 or $500 behind on their monthly bill—or if they manage to scrounge together money to pay it all just a couple days late.

Had the CFPB’s rule stood, late fees charged to families would have likely shrunk by nearly 60 percent in 2025. Since the Trump Administration scrapped that rule, we estimate that families likely paid between $17 billion to $20 billion in additional fees in the first year of his Administration (depending on if revenues stayed steady or increased by the average annualized growth rate from 2020 to 2024, based on data published by the CFPB).

Beyond being good politics for the President, capping credit card interest rates is also good policy. American families can’t afford the sky-high interest rates and junk fees that bank CEOs are draining from them, just for trying to get by. The President has a real opportunity to deliver on one of his signature campaign promises and bring down costs for millions of families by billions of dollars each year. The only question that remains: will President Trump follow through, or will he cave to Wall Street once again?

To learn more about how capping credit card interest rates can yield major savings for American families, check out the following:

- For a comprehensive report on the feasibility and savings to working families from a credit card interest rate cap, read this groundbreaking report by Brian Shearer, Director of Competition and Regulatory Policy at the Vanderbilt Policy Accelerator. He finds that credit card banks’ profit margins are more than wide enough to comfortably absorb an interest rate cap, and a 10 percent cap will put billions of dollars back into Americans’ pockets with minimal impacts upon rewards and lending volumes—saving the average person $899 every year.

- For Brian’s response to a purported rebuttal by the American Bankers’ Association, check out his “take-down.”

- For a deep dive into how the Trump Administration’s own CFPB published research further confirming that American families need financial relief from interest rates, take a look at last week’s Substack article by Mike Pierce.

###

This Protect Borrowers blog was also published on In Debt, a Protect Borrowers Substack.