In 2026, We’re Making Bank Executives the Villains Again

By Mike Pierce | January 8, 2026

As working families struggle to stay afloat, rising prices and ballooning credit card debt present a golden opportunity for some of the biggest banks in the world to do what they do best—jack up fees and interest rates on their customers, and rake in record profits. This comes as JP Morgan Chase CEO Jamie Dimon and Capital One CEO Richard Fairbank brought home record-setting salaries and bonuses, as these banks’ boards paid special recognition to just how effective Dimon and Fairbank have been at gouging working people who are falling further and further behind.

A new report from the Trump Administration’s own Wall Street watchdog—the embattled Consumer Financial Protection Bureau (CFPB)—lays bare just how fat credit card banks have grown off the record-smashing charges imposed on their customers, many driven deeply into credit card debt to pay for groceries, healthcare, and housing.

By Christmas, credit card bank executives had everything on their wish list.

But first, some context. The Trump Administration has rolled back rules intended to lower credit card late fees, ended routine supervision of the biggest banks in the world, and greenlit a mega-merger between Capital One and Discover, creating the largest subprime credit card issuer on the planet. Working class voters remain on edge as they wait to see whether the President will deliver on his marquee campaign promise to lower costs: his bipartisan pledge to cap credit card interest rates at ten percent.

In Trump’s economy, what is good for bank executives is bad for borrowers. In the waning hours of 2025, the CFPB quietly published a damning new study that looks at the business practices and market conditions underpinning Americans’ historic levels of unaffordable credit card debt. This study offers a snapshot of the credit card market at the dawn of the new Trump Administration and tells a story about American families’ debts, illustrated with data from the largest credit card banks.

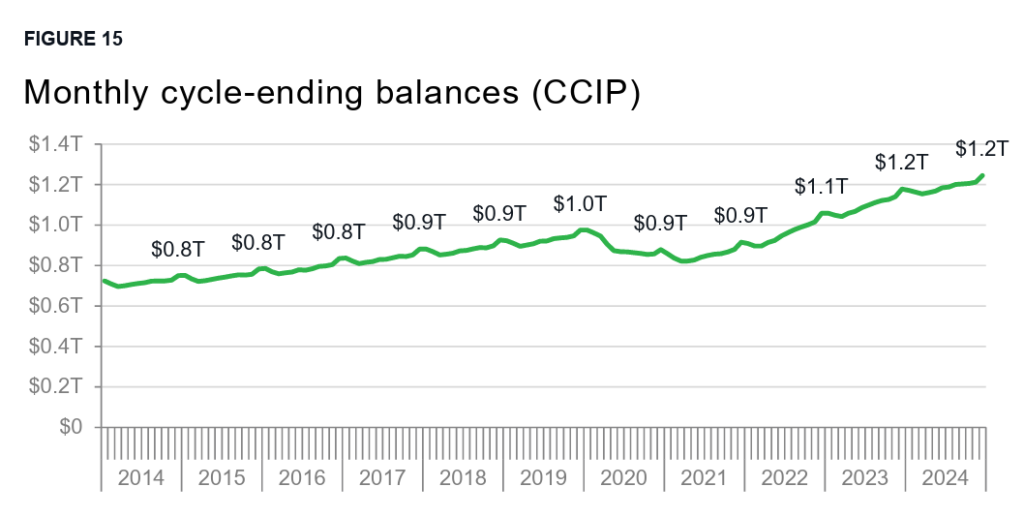

The upshot: Americans owe the most credit card debt in at least a decade and are paying banks the most money ever recorded in credit card interest charges and fees.

My colleague Brian Shearer at Vanderbilt Policy Accelerator made a similar observation about the shocking volume of credit card interest charges repeatedly over the past few months—drawing feigned outrage from the same bank lobbyists (here’s his “Take-Down” in response).

Now we know that the Trump Administration’s own, embattled consumer watchdog has a similar view of the dynamics at play and the strain that high-rate, high-fee credit card debt poses for working families. This report is worth reading in full, but the main points on credit card interest charges are stunning:

- Americans paid more than $160 billion in credit card interest charges in 2024—a 50% jump since 2022. The CFPB’s study notes that this is the most Americans have paid in credit card interest charges since at least 2015.

- Half of all credit cardholders “revolve” a balance and are exposed to sky-high credit card interest rates. The CFPB observed that the share of revolvers at the end of 2024 had climbed back to pre-pandemic rates—ending a brief decline in the share of Americans who could pay off a credit card balance each month.

- It was much more expensive to owe credit card debt in 2024 than it was in 2022. As CFPB explains: “Annual interest charges since 2022 grew 52 percent, but the number of cardholders only grew by 9 percent. That represents an additional $45 billion in interest charges not explained by growth in accounts.”

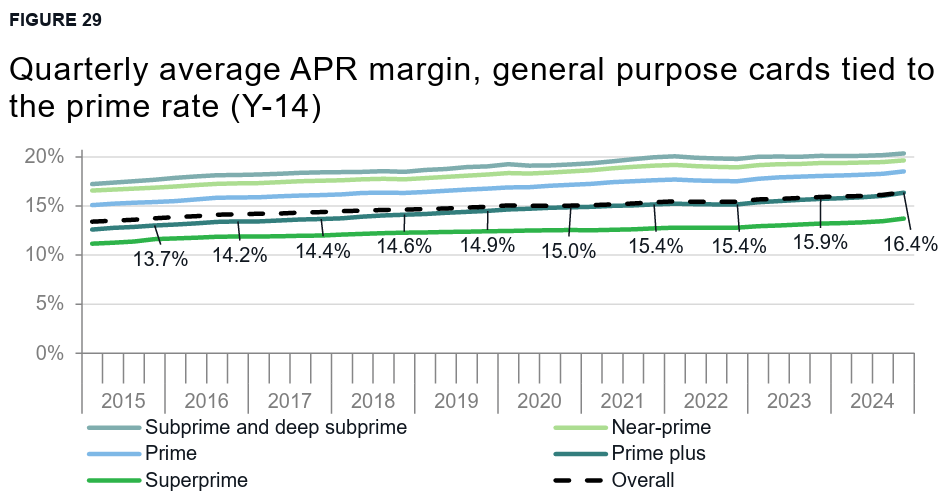

Further into this study, the CFPB looks at the spread between the prime rate (the benchmark typically used to determine changes in credit card interest charges) and the actual Annual Percentage Rate (APR) charged to Americans who owe credit card debt. This spread offers a rough gauge of how lucrative the credit card business is for these banks.

Last year was a great time to be a credit card banker.

As President Trump took office, a typical credit card had the widest spread between the prime rate and the APR charged to cardholders in the decade since the CFPB started tracking this indicator. That means that every dollar of Americans’ credit card debt made more money for a credit card bank in 2024 than it has at any time on record.

Credit card banks made gargantuan, windfall profits by opportunistically raising *APR margins* when everything got more expensive and then keeping those *margins* high even when borrowing costs dropped. The CFPB offers us a clear, tight rebuttal to the bank lobbyists’ favorite talking point—that high rates are just a function of high borrowing costs for banks. This does nothing to explain the upward growth in APR margins, which appears to just be good old-fashioned corporate greed.

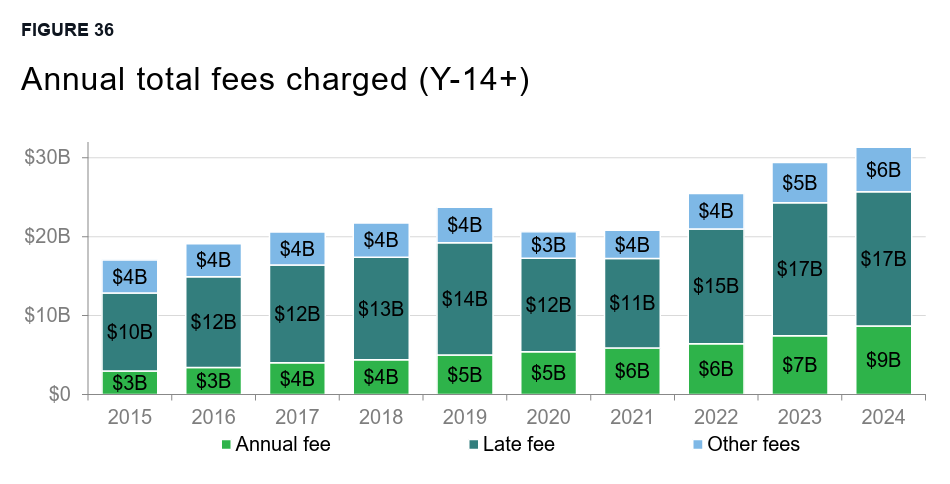

Data shows a credit card industry addicted to junk fees.

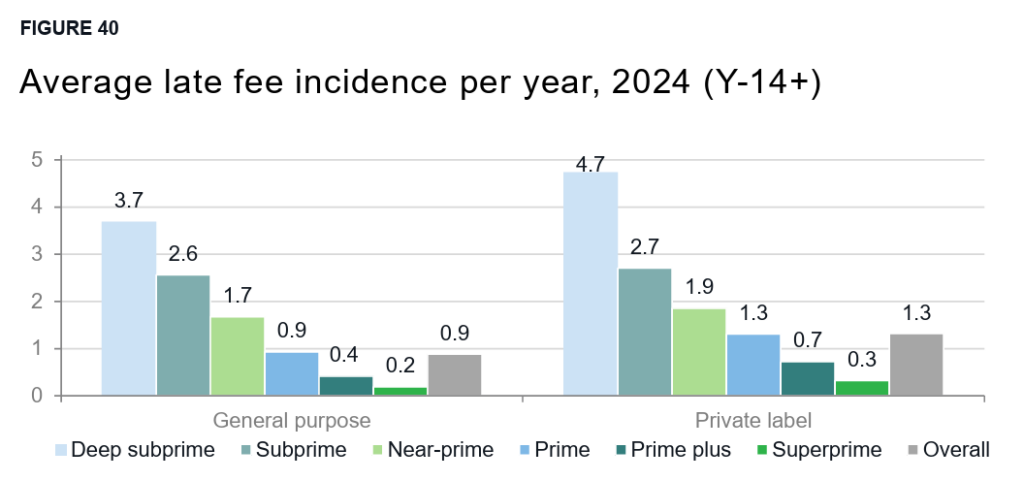

As President Trump came into office, credit card banks were engaged in a pitched courtroom battle to block a Biden-era CFPB rule that would have capped credit card late fees at $8—saving the average family $220 each year and working Americans more than $10 billion annually. Last April, Trump’s CFPB cut a back-room deal with these banks and agreed to axe these new limits on junk fees.

At the time, we knew this would produce windfall profits for the biggest banks. The CFPB’s study sharply confirms that intuition—they found that families paid more than $30 billion in credit card fees in 2024, a 25 percent jump over 2022 levels and the highest volume of fees ever recorded. Late fees comprised the largest chunk of this record-smashing fee revenue—American families paid $17 billion in late fees in 2024, up more than 13 percent since 2022.

Let’s also not forget that fees are only one of many ways that credit card bankers make money. In 2024 alone, these banks also raked in $160 billion in interest rate charges and roughly $149 billion in credit card swipe and interchange fees. Combined, that’s over 18 times what they make in late fees. As my colleague Brian Shearer notes, the return on assets (ROA) on credit cards is nearly six times the return for all banking activities—meaning that credit cards are an extremely lucrative business. All of that is to say, capping or even eliminating credit card late fees barely makes a dent in card banks’ balance sheets (despite what lobbyists claim), but for individual families it could mean the difference between breaking even at the end of the month or skipping meals, forgoing medical care, being late on rent, or taking out a payday loan.

Of course, Trump’s CFPB doesn’t acknowledge its own role in this mess. Had the CFPB implemented its late fee rule instead of surrendering to the credit card banks, we would have expected 2025 late fee revenue to fall by nearly 60 percent (this is my math, feel free to check me on it if I’m wrong, ABA). Donald Trump, Russ Vought, and the team fighting to dismantle CFPB successfully protected a driver of credit card banks’ profits—even when it will disproportionately hit working class Americans with deep subprime and subprime credit scores.

While we’re on the subject of corporate greed, there are a couple of big, below-the-fold stories in the CFPB study that all push in the same direction. Highlights include:

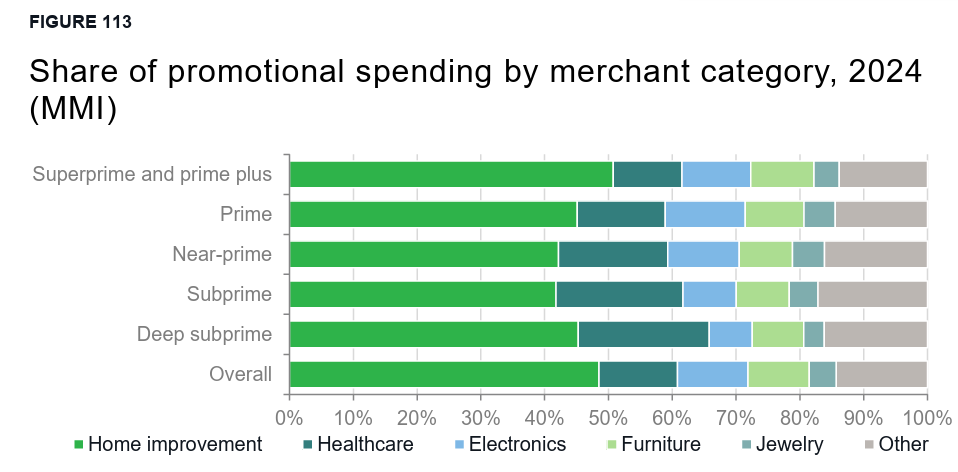

- Credit card debt is medical debt. As the CFPB explains, healthcare spending on credit cards climbed 50 percent between 2019 and 2024, approaching $200 billion per year. Over this period, health insurance deductibles grew rapidly—leaving working families with more out-of-pocket healthcare costs than ever before. Americans with weaker credit are also increasingly using deferred interest promotional offers from credit card issuers to cover their healthcare costs. This is another “K-shaped economy” story—in 2024, Americans with the strongest credit used credit card promotional offers to fix up their homes, while Americans with the weakest credit used promotional offers to access healthcare.

- As online sports betting booms, credit cards are fueling America’s gambling habit. Spend some time on gambling Reddit and you’ll see the ugly face of Americans’ new embrace of online sports betting—gamblers desperate for access to credit in order to keep betting. As we’ve written about for IN DEBT, the face of American sports bettors is men under 45, who gamble more frequently online and go into debt at far higher rates than the rest of the population– the same voters who tipped the scales for Trump in the 2024 election.nThe CFPB sees a surge in gambling debt in its 2024 credit card data, too. As the Bureau notes, “gambling spending on credit cards is low but growing—in 2024 it was $2.7 billion, nearly double the $1.4 billion it was in 2019.”

Across these observations, one thing is clear: the credit card industry has embraced a business model that exploits America’s affordability crisis, extracting record finance charges and fees from families trying to stay afloat. There has been a lot of speculation about how the real profit center for the credit card banks is swipe fees—the transaction costs that businesses shoulder and that allegedly pay for increasingly generous rewards programs that cater to the wealthiest cardholders. There is some truth to this, I’m sure, but the CFPB report paints a different picture—from widening APR margins and targeted offers to finance healthcare to the surging share of Americans revolving credit card balances, we see an industry trying to drive working people into debt and keep them in debt over the long term.

Trump’s CFPB shows us that reining in credit card banks is central to any serious affordability agenda—something President Trump’s own campaign recognized. Unfortunately, the Bureau is afraid to do anything about it because Russ Vought cares more about banks than people. SAD!

###

Mike Pierce is the Executive Director of Protect Borrowers. This blog was also published on In Debt, a Protect Borrowers Substack.