With Gig Worker Cash Advance Our Broken Labor Market Brings Desperation Finance to Work

By Chris Hicks | June 25, 2026

As tens of millions of American households grapple with the rising cost of everything, more and more are falling into debt just to make ends meet. That’s not by accident. As we discussed last week, firms from Wall Street to Silicon Valley are increasingly—and aggressively—preying on Americans’ desperation by popping up on our phones to offer us quick cash now.

Desperation finance targets the gig economy head-on, offering a new set of high-cost financial products that exploit gig workers’ supposed legal status as independent contractors. “Gig Worker Cash Advance”—an umbrella term for the shady credit pushed on gig workers— relies on jargon and endless tricks to hook gig workers into loans with rates that pencil out to more than 2,000 percent APR. It’s just new packaging for an old business model—loan sharking to exploit workers desperate for a little more cash just to get by.

Desperation and the Gig Economy

The tech platforms powering the gig economy—including DoorDash, GrubHub, Instacart, Lyft, Rover, Shipt, TaskRabbit, and Uber—emerged in the early 2010s in Silicon Valley. These corporations built apps to connect customers and workers in real time, facilitating transportation, food delivery, home rentals, and more. The use of these platforms exploded in the US, starting as small test pilots in a few cities and leading tens of millions of Americans to regularly use them within just a few years. By the end of the first decade of their existence, a number of these companies went public, raising hundreds of billions of dollars from retail investors.

These companies really want you to believe that this new technology isn’t just good for their customers, but that it facilitates “flexible” work that is good for gig workers too. Just read this New York Times op-ed from Uber’s CEO:

“[T]his is because [gig workers] understand the trade-offs between traditional employment and app work. Unlike traditional jobs, drivers have total freedom to choose when and how they drive, so they can fit their work around their life, not the other way around.”

As of early 2026, an estimated 57 to 70 million Americans participate in the gig economy, representing roughly 36 percent of the U.S. workforce. For too many of these workers, promises of flexibility and freedom proved too good to be true. Many earn less than minimum wage. Poverty-level incomes mean that their financial lives are incredibly precarious; they live paycheck to paycheck, one accident or illness away from financial disaster. When a financial disaster arrives—when life happens—there is no safety net in place to catch them.

Ed. note: workers, unions, and advocates have fought for years to make the case that these workers are not independent at all and are, in fact, misclassified as “contractors” to the benefit of these platforms and in violation of federal, state, and local labor laws. For more on the fight to win workplace justice for gig workers, see worker organizations like Los Deliveristas Unidos and Rideshare Drivers United, and National Employment Law Center’s “Fighting the ‘Gigification’ of Work.”

Why Loan Sharks Love Commercial Lending

At the same time as the gig economy was taking off, Wall Street was emerging from its darkest days in nearly a century. Historic financial institutions had been wiped out, the stock market had cratered, and credit had dried up. As a result of the 2008 financial crisis, traditional banks severely tightened their lending standards and stopped offering small-dollar business loans. This created a void that left many small businesses desperate for short-term capital in search of a financial lifeline, and they found it in a largely unregulated corner of the financial world: Merchant Cash Advance (MCA).

Beginning in the early 2010s, this industry experienced rapid growth. And this rapid growth mostly went unchecked and unregulated. This was the MCA industry pitch: we do not need to follow the law because we are not making loans. Instead, firms describe these financial products as revenue-based financing or selling you your future income today. They claim that if your business earns more, you’ll repay more. If you earn less, you’ll repay less. But in most instances we’ve uncovered, that is pretty far from what most borrowers experience. Most come with a fixed payment schedule and a fixed payment amount. In other words, an MCA is functionally just a loan.

These lenders have also tried to use fine print and exotic terms to obscure these financial products’ status as something other than loans. For example, these firms charge so-called “factor rates” rather than interest rates. But these word games do not hold up upon closer scrutiny. Here is how a factor rate works: Total Repayment = Advance Amount × Factor Rate. For example, if a small business borrows $10,000 with a factor rate of 1.6, they will have a total repayment of $16,000 ($10,000 × 1.6 = $16,000). You don’t have to look very hard to find many calculators that can convert “factor rates” into their equivalent APR or interest rates. But what a “factor rate” does accomplish: hiding the outrageous cost of borrowing money.

Little is known about this market because the industry effectively exploits gaps in oversight—lenders are nonbanks and they purport to engage only in business lending, not consumer lending—a weak spot for state and federal financial regulators. Some analysts estimate the US market size of MCAs to be around $20 billion, and expect it to eclipse $30 billion by 2031 (for comparison, the payday loan market was $37.28 billion in 2025).

These firms offer products with a toxic mix of traits—exotic terms that mirror the worst of Wall Street, paired with mafia-style debt collection tactics and usurious interest rates.

Earlier this month, More Perfect Union talked to New York Attorney General Tish James about the squeeze these firms put on the smallest businesses.

Doubling Down on Exploitation

This is where our two stories meet. And once again where gig workers get screwed.

At least according to the platforms that dole out gig work to tens of millions of Americans, gig workers are legally independent contractors—each gig worker is effectively classified as a small business. When gig workers face financial disaster due to an illness or accident, there is no social safety net to catch them and banks often won’t lend to them because they lack W-2s to prove their credit history and worthiness.

That is where MCA lenders come in. There are a growing number of these firms eager to offer gig workers tied to the biggest platforms—Uber, Lyft, Instacart, GrubHub, DoorDash, and many more—a cash advance, even going as far as targeting a line of these products specifically to gig workers: Gig Worker Cash Advance.

Loan sharks are targeting gig workers with a simple message: you need money in order to make money, and we are the ones here to help you. It’s not quite the same pitch as so-called “Earned Wage Access” or “Earned Wage Advance,” and it’s not quite a payday loan. It has all the worst features of both and more. To understand just how bad this is, and what these workers are experiencing, I want to walk you through these products that are actively being sold to gig workers struggling to make ends meet today.

Common features of Gig Worker Cash Advances include:

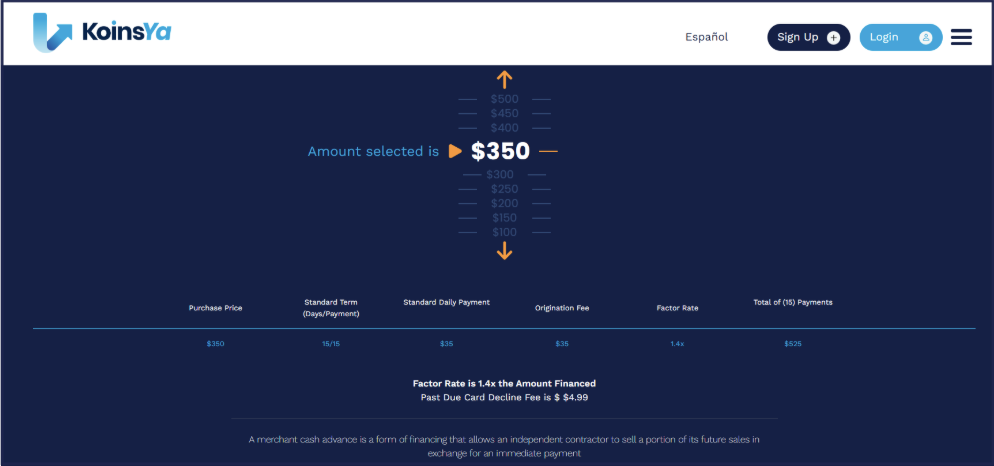

- Eye-popping Interest: KoinsYa is a merchant cash advance lender that targets gig workers and their website provides a helpful view into this market. While the “Rates” section on their website is laid out in increments of $50, we are able to see how their math works: If you borrow $380, you have a standard daily payment of $38, an origination fee of $38, a factor rate of 1.4, and you pay that daily over 15 days. Now if you plug those numbers into NerdWallet’s Merchant Cash Advance Calculator, you will find that KoinsYa is offering gig workers a whopping 2,381% APR interest rate. It will cost you $190 in finance charges to borrow $380 for 15 days.

- Unrelenting Collections: The vast majority of these gig worker cash advance companies require gig workers to connect their bank accounts with the cash advance lenders via ACH—which allows these lenders to automatically withdraw funds from workers’ bank accounts. Cash advance lenders do this to skip the line and ensure they collect as much cash as possible in the event that a gig worker or business declares bankruptcy. One cash advance company called Giggle Finance (yes, this is their name) has faced numerous complaints from borrowers about withdrawing funds immediately when banks open, sometimes pushing gig workers to overdraft on their accounts, and performing multiple withdrawals in a single day—sometimes as many as 10 attempts in a day. This practice also makes matters worse by pushing workers into stacking cash advances to pay off previous loans borrowed, throwing gig workers into a spiral that can be impossible to escape.

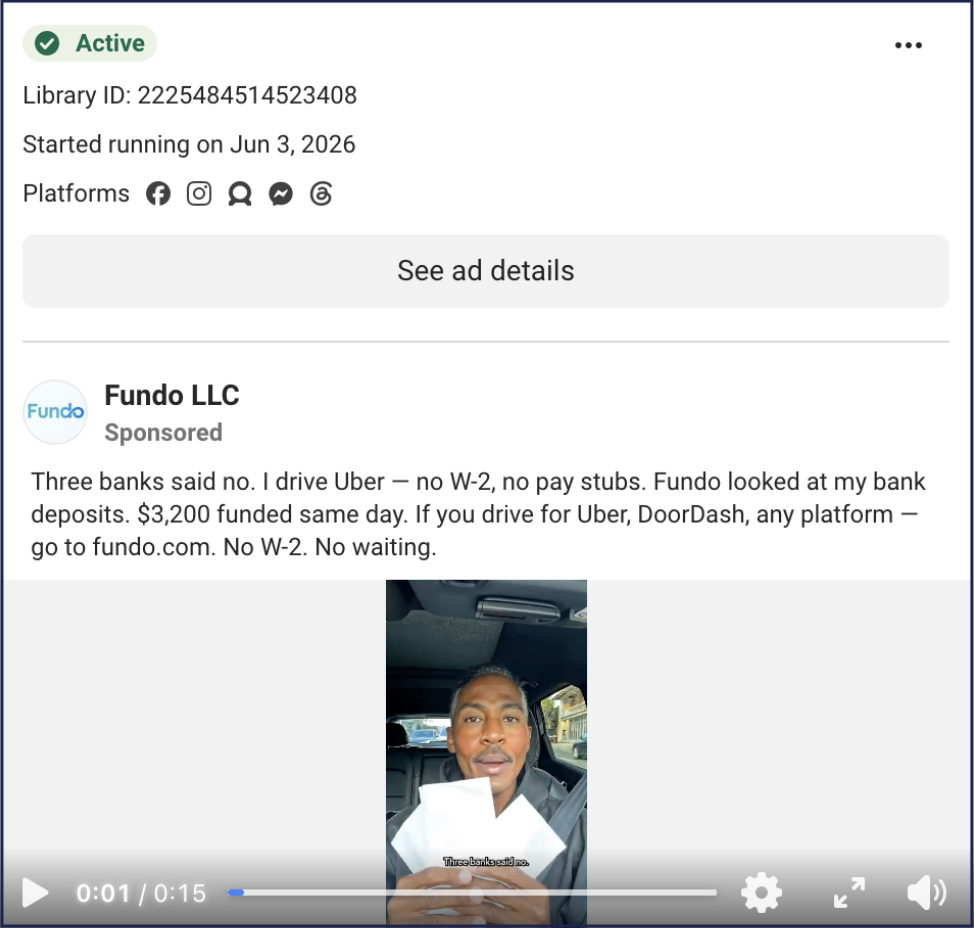

- Abusing Liens to Force Repayment: One of the common complaints by gig workers about one MCA lender called Fundo is their heavy reliance on a debt collection tactic called a “UCC lien” that prevents workers from accessing their own money. A “UCC lien” is a lien filed with a state government where a creditor can prohibit a business from accessing an asset or property until a debt is repaid—in these cases the “business” is a gig worker and the “business asset” is a bank account or digital wallet where the gig worker gets paid. In our initial investigation into both Fundo and Giggle Finance, we found thousands of examples just from Colorado, Ohio, and Pennsylvania of these two companies filing UCC liens against gig workers’ bank accounts, CashApp accounts, and accounts they are paid into by the gig platforms themselves. These UCC liens can last for years, and some gig workers report the only way to have the MCA lender remove the lien and regain access to their own money is to pay an inflated paperwork filing fee that can cost hundreds of dollars.

- Harvesting Junk Fees: There are numerous complaints against the largest gig worker cash advance companies for applying processing fees, expedited transfer fees, fees for turning off automatic ACH withdrawals, fees for filing paperwork to stop UCC liens against banking accounts, and subscription fees. These junk fees can lead to gig workers in desperate need of financial assistance worse off than if they had never taken out these loans to begin with.

This is the experience gig workers face when they turn to a Gig Worker Cash Advance in a moment of desperation. These Gig Worker Cash Advances are marketed as “not a loan” but they are among the most shocking examples of predatory lending across the American economy.

We Have the Tools to Begin to Rein in This Harmful Industry

A number of states already have the tools at their disposal to begin to treat these merchant cash advances and gig worker cash advances for what they are: loans.

That should include:

- Require merchant cash advance and gig worker cash advance lenders to become licensed and registered to operate, bringing them under the supervision of state regulatory agencies.

- Apply relevant financial protection to these loans, including usury limits, consumer fraud and fair debt collection practices, truth in lending acts, and rules against unfair or deceptive acts and practices.

These steps are urgent and necessary but not sufficient to deal with the threats gig worker cash advances pose to workers themselves and to the broader economy. Across the country, predatory lenders exploit the perception that business lending offers a free pass to evade basic rules that protect individual borrowers. If a financial product hides its true costs, harvests junk fees from desperate customers, and tricks users into paying more than they owe, then law enforcement officials and financial regulators should immediately and aggressively act to protect borrowers. If they determine they lack the legal tools to do so, state and federal lawmakers need to change the law. A fair economy should encourage consumers, workers, and small businesses to access credit and flourish, free from deception and abuse.

###

Chris Hicks is a senior policy advisor at Protect Borrowers. This blog was also published on In Debt, a Protect Borrowers Substack.