This Was Always the Plan but Regulators Shouldn’t Accept It

By Mike Pierce | May 7, 2026

This financial aid season, private student lenders are expanding loan options for graduate students to address financing gaps caused by the One Big Beautiful Bill Act. As we’ve warned over, and over, and over, and over again, the private student loan industry has no interest in replacing the broad public mission of the federal student loan program— ensuring access to a higher education regardless of race or economic status. Instead, private student lenders are gleeful about the opportunity to target new lending to a small slice of higher education, consequences be damned.

The effects of this are coming into focus: because of policy decisions by President Trump and his Republican allies in Congress, paired with business decisions by private lenders, America’s graduate students will look a whole lot less like the rest of America.

Private student lenders are targeting their booming business on two different dimensions. First, as my colleagues Jenn Zhang and Peter Granville have written, established underwriting practices by the vast majority of the private loan industry will lock out 40 percent of American families from traditional private student loans. Last month, attorney and Protect Borrowers fellow Austin Hinkle wrote a piece looking at the risks posed to students when schools try to build their own loan programs to fill the gaps left behind by these lenders’ underwriting limits. It’s all very bad.

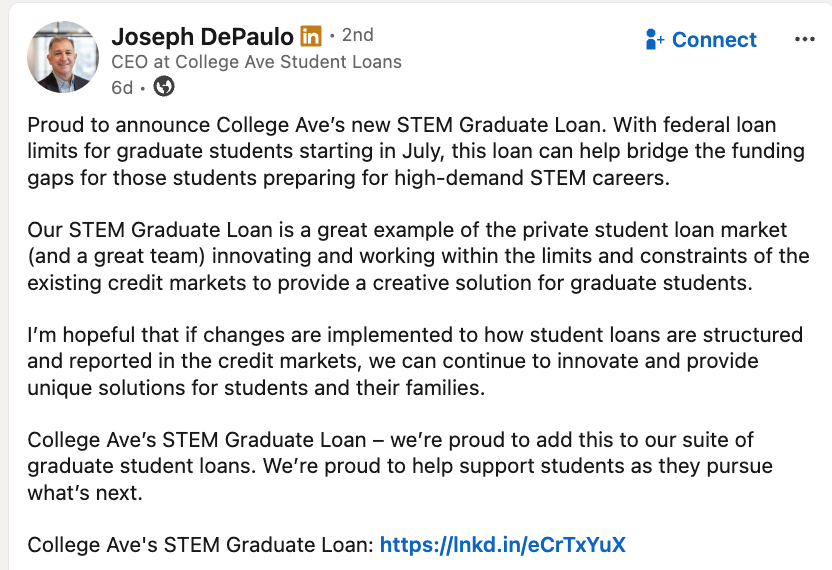

Today we’re looking at this problem from a second angle—what does it mean when private lenders pick specific programs to serve, but do not lend broadly to graduate students? Last week, College Ave’s long-time CEO Joseph DePaulo announced a new loan product limited only to graduate students pursuing “high-demand STEM careers.” As DePaulo explained on LinkedIn, this new product is an example of lenders “innovating and working within the limits and constraints of the existing credit solution for graduate students.”

What DePaulo leaves unsaid is that his solution only provides financing to certain graduate students—namely the overwhelmingly white and male graduate students who pursue STEM careers. This raises significant concerns about how DePaulo’s firm—and the private student loan industry at large—plans to comply with federal and state civil rights and fair lending laws while also targeting loan products to majors where women and Black and Latino students are severely underrepresented.

The private student loan industry has a long track record of targeting loan products and loan terms based on criteria that correlate with students’ race, gender, and national origin. As far back as 2014, the Federal Deposit Insurance Commission cited Sallie Mae for violations of federal fair lending law, ordering it to cease using schools’ “cohort default rates”—a metric that correlates with the enrollment patterns of Black and Latino/a students—to target its private student lending. Just last year, the private student lender Earnest, a business unit of Navient Corporation, settled charges of unlawful discrimination brought by Massachusetts Attorney General Andrea Campbell. In this matter, the Massachusetts AG alleged that Earnest’s:

“…lending practices violated various consumer protection and fair lending laws, including through the use of artificial intelligence (AI) models that could lead to disparate harm to Black, Hispanic, and non-citizen applicants and borrowers.”

Federal and state fair lending and civil rights laws prohibit discrimination against consumers from specific protected classes. Public comments from private student lenders and trade associations—including College Ave’s new STEM loan product—suggest that the race to deploy new private student loan options for graduate students may result in the same unlawful discrimination that has been the focus of actions by enforcement officials and financial regulators for more than a decade.

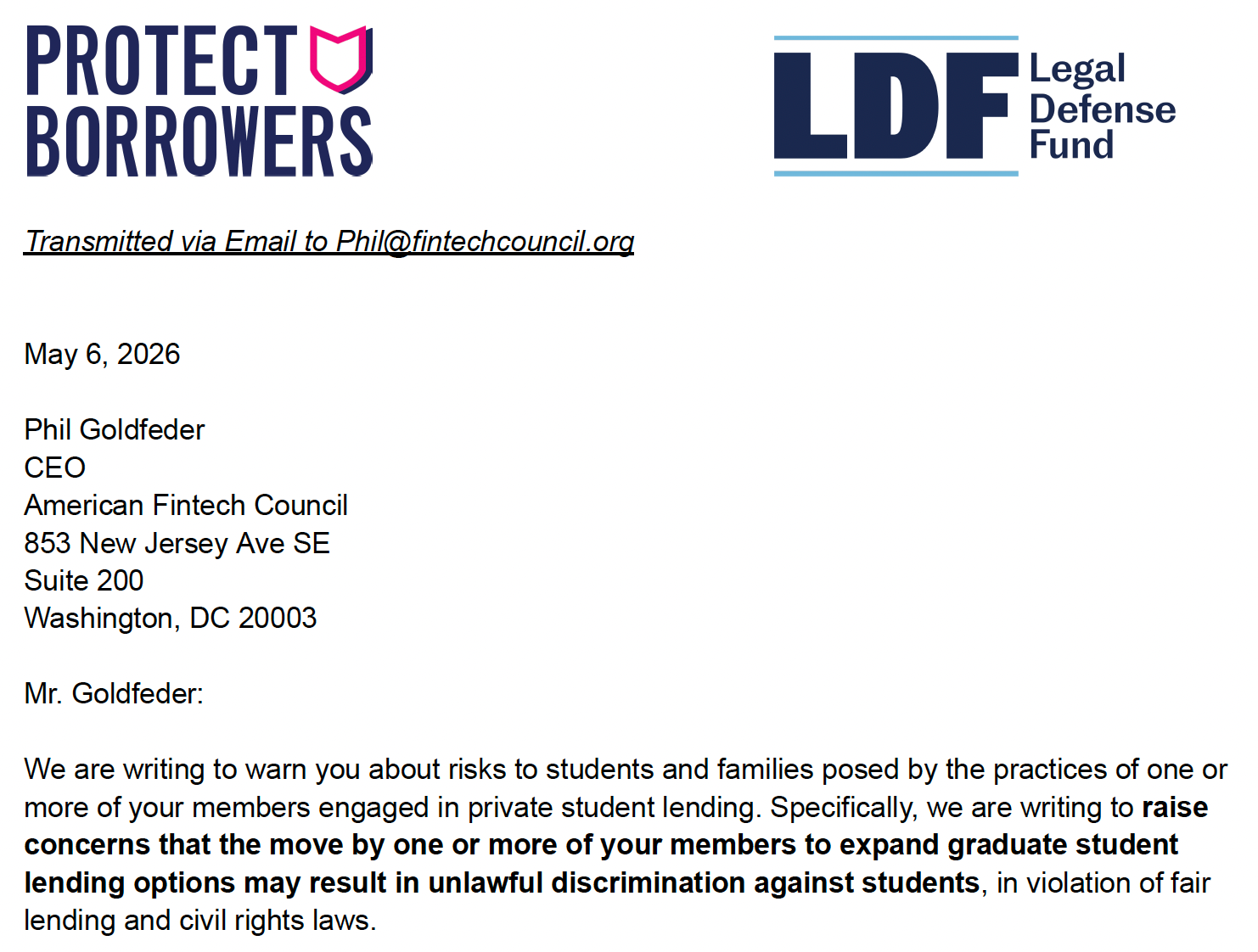

Yesterday, we, along with our partners at NAACP Legal Defense Fund, sent a letter to the American Fintech Council (AFC)—the DC trade association that represents both Earnest and College Ave—asking some basic questions about how AFC members are managing fair lending risk as they roll out these new programs. AFC’s members have a track record of “educational redlining” and it appears that, despite a public commitment to “advance standards of fairness and nondiscrimination,” at least some of their members are doing the opposite.

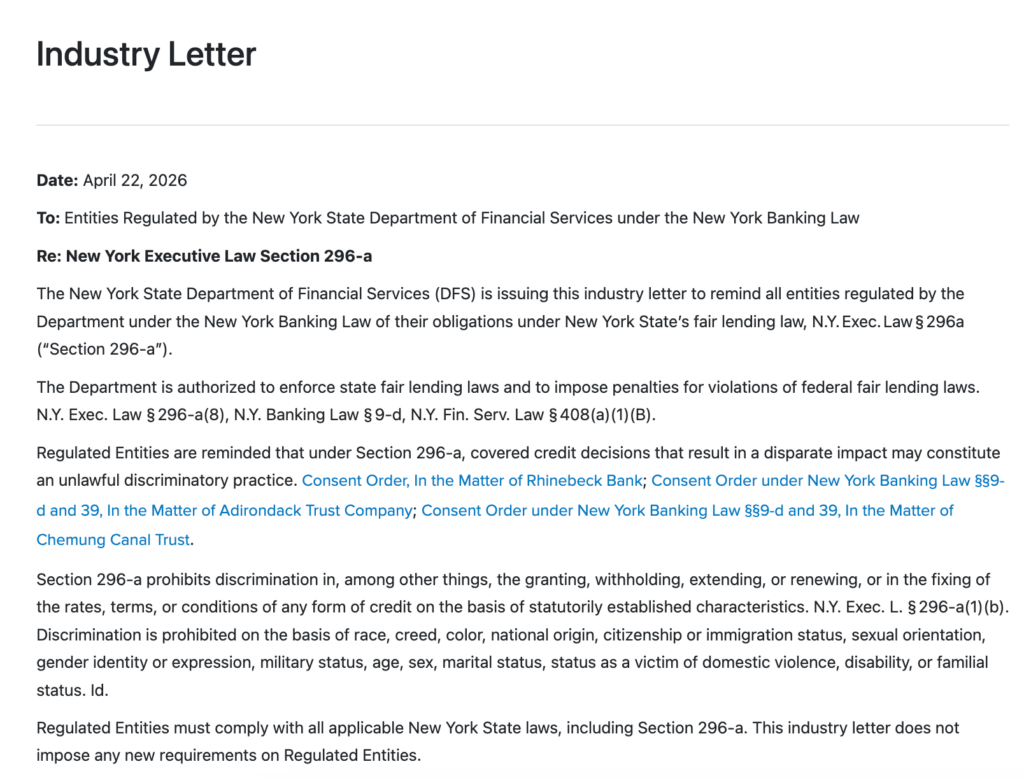

Private student lenders’ shift in lending practices comes at a precarious moment for the future of federal fair lending law enforcement. As Ben Kaufman wrote on last week, the Consumer Financial Protection Bureau (CFPB) published a new—and seemingly illegal—interpretation of the Equal Credit Opportunity Act that throttles efforts to hold financial firms accountable for practices that have a “disparate impact” on borrowers from protected classes. On the heels of CFPB’s retrenchment, New York’s Department of Financial Services made it clear to the firms it regulates—including College Ave—that it expects the financial services industry to comply with state fair lending law and, specifically that “covered credit decisions that result in a disparate impact may constitute an unlawful discriminatory practice.”

Schools and lawmakers all shoulder some blame for an emerging status quo that will deny access to a graduate degree to millions of students over the next decade. What happens next is still uncertain, but today one thing is clear: the private student loan industry is an active partner in the right-wing effort to slam the doors to higher education in the face of working class students, especially Black, brown, and female students.

For more analysis of the One Big Beautiful Bill Act’s caps on federal student aid and the risks for students in the private student loan market, check out this piece from our friend Eileen Connor at the Project on Predatory Student Lending on Inside Higher Education.

Rhetoric from executives about expanding access to higher education is misleading—there is no altruistic motive here. The private student loan industry remains relentlessly focused on maximizing its profits amid this enormous shift in lending and borrowing across American higher ed.

###

Mike Pierce is the Executive Director and co-founder of Protect Borrowers. This blog was also published on In Debt, a Protect Borrowers Substack.