BNPL lenders are taking advantage of Americans’ financial desperation. It’s time for a BNPL Borrower Bill of Rights.

By Jennifer Zhang | July 13, 2026

Imagine a loan product where half the borrowers have missed a payment in the last year, two-thirds have subprime credit, the bill comes due every two to four weeks, and the penalty fees for falling behind can rival a 200 percent APR. Does it sound a bit like a payday loan? Now imagine that the same product appears everywhere you shop—nearly every online storefront, most major grocery stores, the wallet app on your phone—and that somewhere around half of adult Americans have used it.

But it’s not a payday loan. It is a product marketed as Buy Now, Pay Later (BNPL).

This is all happening right now amid a worsening affordability crisis, a stagnant job market, the friendliest administration to Wall Street and Silicon Valley in a generation, and a growing trend of desperation finance: where lenders and fintechs capitalize upon families’ desperation when buying food, paying rent, or purchasing other essentials and push them into debt.

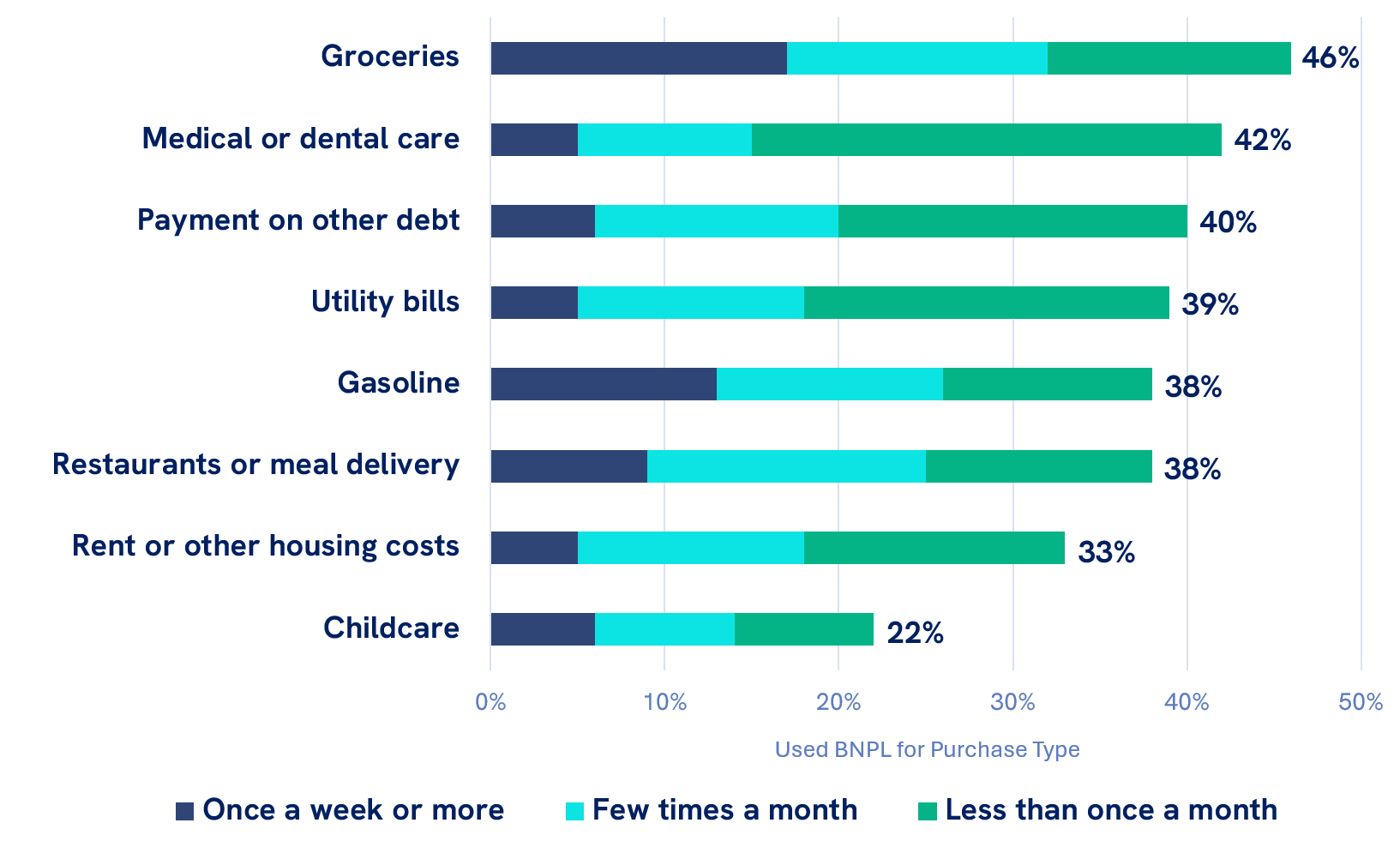

Survey shows more Americans are using BNPL to cover the basics. They want policymakers to rein in abuses in the BNPL market.

We partnered with Data for Progress on a new survey exploring the experiences of American voters with BNPL products. According to our poll, nearly half of BNPL users have used the product to help pay for groceries (46 percent). Between just over a third to nearly half of users have used BNPL to pay for medical or dental care (42 percent), other debt (40 percent), utility bills (39 percent), gasoline (38 percent), restaurants or meal delivery (38 percent), and rent or other housing costs (33 percent). Over 1 in 5 users (22 percent) have used BNPL to pay for childcare.

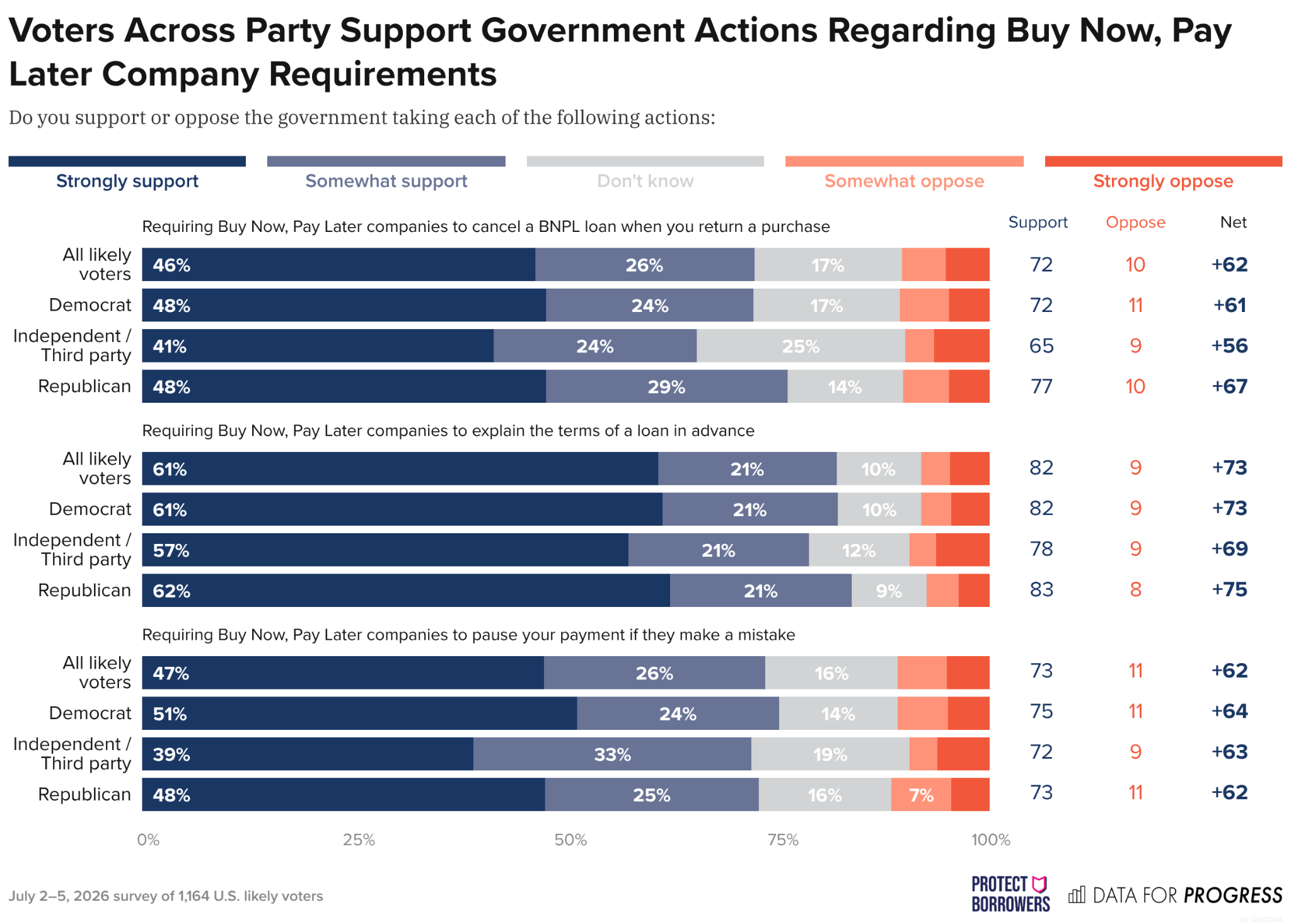

As Americans increasingly rely on these products, they want common sense protections. The poll also showed that a supermajority of voters across party lines support policy action to rein in predatory and harmful practices in the BNPL market.

We dug into the rapid expansion of the BNPL market and the unique harms BNPL loans pose to working families.

Today, we released A Loan In Every Cart, the most comprehensive report on the BNPL industry to date. We found that, contrary to how the BNPL industry has marketed itself, its loans are anything but “interest-free,” and are designed to obscure the cost of financing for borrowers. On top of that, millions of Americans have turned to BNPL precisely because their paychecks can’t keep up with the skyrocketing cost of living, and they need to find a way to pay for groceries, car repairs, medical bills, and other necessities. But BNPL debt isn’t like your typical personal loan. Here’s what we found:

- BNPL loans are packed to the brim with junk fees. In fact, the business model depends upon junk fee churn. Unlike a credit card, personal loan, or even typical payday loans, BNPL financing is largely designed as one loan per transaction. Every grocery purchase, every overdue bill, and every merchant transaction leads to the origination of a new loan. If you use BNPL to finance just a portion of your grocery bill and you buy groceries once a week, that means you could take on four loans in just a month, each with payments due every two weeks for six weeks afterward—for a total of 12 payment requests that later hit the bank account. Confused? We get it, and many borrowers lose track too. The consequences are expensive. Being late on any of those payments can lead to a $7 or more late fee, plus potential overdraft or non-sufficient funds fees and other charges from the bank. Some lenders also charge fees for any of the steps a borrower might take to avert a late payment when funds are low, like rescheduling their due date or not setting their bank account as the default method of payment.

- Borrowers who miss payments can end up paying the same as they would for a high-APR, payday loan. We modeled that a borrower who takes out $100 loans for groceries and experiences income shocks could end up paying the same as they would have for a 139 to 208 percent APR loan (from owing $16 to $24 in late fees for six-week terms). That model uses a lender that self-imposes late fee caps of $8 with an aggregate of up to 25 percent of the transaction value—it could get much worse at a lender that doesn’t.

- BNPL lenders are increasingly turning toward interest-bearing loans. Over a third of BNPL loan originations are now interest-bearing, with some lenders relying primarily on interest-bearing loans. Over 1 in 4 BNPL borrowers (28 percent) have taken out longer-term, interest-bearing loans. Increased uptake of interest-bearing loans shows that the BNPL business model of offering pay-in-four loans is working, as borrowers are more likely to come back for future, more expensive financing of potentially larger purchases. It also may reflect that financial strain is pushing borrowers to take on interest in exchange for lower monthly payments.

- BNPL lenders are doing a lot more than just making BNPL loans—they’re breaking into banking and credit card issuing, and even pushing products through artificial intelligence (AI)-powered chatbots. Users can pay for purchases at any merchant on the Visa network using a BNPL loan (thanks to single-use and digital cards), but BNPL lenders are also partnering with Visa and chartered banks (and in some cases, applying for bank charters themselves) to issue credit cards, debit cards, and bank accounts. They are also engineering new ways to induce people to take on debt, such as by integrating their offerings into AI chatbots like ChatGPT and Gemini. It is critical that regulatory conversations catch up to market realities, and that law enforcement agencies stay alert as these lenders break into already very well-regulated financial product markets with established rules and strong consumer rights, and push the envelope on fintech-powered finance.

- Women and Black and Latino/a Americans are overrepresented among those who rely upon BNPL. Nearly 1 in 4 Black women and Latinas have used a BNPL loan. Black and Latino/a Americans are about twice as likely to use BNPL, compared to other groups. The disproportionate reliance upon BNPL among women and communities of color likely reflects the ongoing influence of wealth and income gaps by race and gender.

- The spread of BNPL ultimately raises costs for everyone, including Americans who don’t use BNPL. Most BNPL lenders charge a merchant fee of up to 6 percent plus some fixed amount (usually 30 cents) on every transaction. This is between double to nearly 10 times the cost of payment processing for debit cards and credit cards. As BNPL uptake increases, merchants will increasingly pass the costs of these fees onto all customers by raising prices.

What should policymakers do?

BNPL loans are expensive and risky, and often worsen financial outcomes for borrowers who come to rely on them to make ends meet. However, millions of Americans are being driven into these debt products just as they’re trying to get by. Prices are soaring and show no signs of coming down anytime soon. At the same time, the job market is stagnant and real wages are falling. As a result, consumer debt delinquency rates have not been this high since the peak of the Great Recession. As families max out their credit cards and fall behind on other forms of debt, many are turning to BNPL and other predatory, short-term debt products in order to pay for essential necessities. Americans need help. Here’s what we recommend:

- It’s time for Congress to pass a BNPL Borrower Bill of Rights. Policymakers should codify sweeping protections that end deceptive pricing, bring down the cost of BNPL debt, ban predatory practices that harm consumers, and empower Americans to enforce their rights under the law. We outline over a half dozen specific policies and rules to provide these protections in our report.

- Congress should compel the Consumer Financial Protection Bureau (CFPB) to do its job. The CFPB is the only federal financial regulator with direct supervisory authority over non-bank financial lenders like BNPL lenders and fintech firms, but under the Trump Administration, the CFPB has been gutted and abandoned its obligation to protect Americans. Congress should compel the CFPB to use its research, regulation, supervision, and enforcement tools to comprehensively regulate the BNPL industry, and fully restore its funding to help ensure its success.

- States should also enact BNPL Borrower Bill of Rights laws and regulate BNPL lenders the way they regulate other lenders: through licensure, supervision, and enforcement. States should require BNPL lenders and their fintech partners to obtain licenses before engaging in BNPL lending to their residents, empower their financial regulator to regulate the market; and exercise their authority under the federal Consumer Financial Protection Act to enforce against lenders that commit unfair, deceptive, and abusive acts or practices.

- States should guarantee BNPL borrowers a place to turn for help. States should establish a dedicated Borrower Advocate office, with the authority to help borrowers struggling with BNPL debt and other products offered by BNPL lenders.

###

Jennifer Zhang is a Policy, Research, and Data Analyst at Protect Borrowers. She was previously a Director’s Financial Analyst at the CFPB, where she worked with the Student Loan Ombudsman’s office, the Policy Planning & Strategy team of the Director’s front office, and the Quantitative Analytics team of the Enforcement Division. This blog was also published on In Debt, a Protect Borrowers Substack.