From Maine to Mississippi, Working Families Are Drowning in Rising Prices and Credit Card Debt

By Aissa Canchola Bañez and Gerardo Bonilla Chavez | July 1, 2026

We are in the midst of summer and as heatwave after heatwave rolls across the country, millions of Americans are struggling not just with the rising temperatures, but also the increasing pressure of credit card debt.

The Federal Reserve Bank of New York recently released a household debt report showing that the number of Americans falling severely behind on their credit card payments has spiked—delinquency rates climbed to over 13 percent in the first quarter of 2026. Delinquency rates haven’t been this high in over 15 years, or since the peak of the Great Recession. If current trends continue, rates may surpass the recession peak before the end of the year.

Working families are in free-fall. Squeezed by a rampant affordability crisis, stagnant wages, and the worst job market since the start of the pandemic, millions of Americans are turning to high-cost credit card debt just to keep the lights on, put food on the table, and cover other basic essentials. The Century Foundation found that over 1 in 3 Americans (37 percent) pay their bills using a credit card, and nearly the same amount (29 percent) have taken on debt to cover basic expenses. About 1 in 4 Americans reported that they or members of their household skipped meals to save money in the last year.

On top of this, a majority of Americans are on the financial brink. Researchers at the Urban Institute found that over half of Americans have no income left after paying their bills each month. Meanwhile, the Ludwig Institute found that over half of Americans wouldn’t be able to cover a $2,000 emergency.

Working families didn’t just end up here by accident. As a result of attacks on unions and organized labor, accelerating mergers and acquisitions between the largest corporations, and skyrocketing income and wealth inequality that produced the billionaire elite, American workers’ real wages have only increased by 29 percent since the 1970s, while the cost of living has skyrocketed by over 580 percent.

When paychecks can’t keep up with the bills, people are forced to turn to debt.

No one is more aware of this than Wall Street and Silicon Valley, who have capitalized on the financial desperation of working Americans and flooded the gap with debt products ranging from increasingly higher-interest credit cards, to Buy Now, Pay Later loans, to even “buy now, pay maybe” loans.

The Credit Card Debt Crisis: State by State

Earlier this year, we released a report finding that 111 million Americans—over 40 percent of U.S. adults and over half of all credit cardholders—can’t afford to pay off their credit card bills in full each month and are forced to pay record-high interest.

Credit card interest rates have increased substantially over the years, as credit card banks have more than doubled their profit margins since 2007. As a result, since 2010, Americans have paid a cumulative total of $2.1 trillion in credit card interest. That’s more than all outstanding student loan debt, more than all auto loan debt, and equal to 7 percent of the U.S. GDP last year.

To complement our report on national trends in the surge of credit card debt, we’re now releasing a state-by-state breakdown of where families are struggling the most, and unveiling a collection of fact sheets showing how credit card debt is growing in all 50 states. Here are our topline findings:

- Borrowers in the South are struggling with credit card debt the most. Nearly 1 in 3 borrowers (32.5 percent) in the South are debt-stressed, the highest of any region. Debt-stressed borrowers are those who use more than 30 percent of their available credit, and are much more likely to fall behind on payments. Debt-stressed borrowers in the South have also seen their average monthly payments increase by over 35 percent since 2018, the highest of any region.

- Borrowers in the South are falling faster into high-interest credit card debt than any other region. On average, over 1 in 4 debt-stressed borrowers in the South (26.3 percent) can only afford the minimum payment or less on their credit card bill. The top seven states where the most borrowers are only able to make the minimum payment or less are all in the South.

- Borrowers in the West and across the South have taken on the largest increases in credit card debt since 2018. Average credit card balances in Western states have increased by more than 16 percent, followed by over 15 percent in the South, more than 12 percent in the Midwest, and over 11 percent in the Northeast.

- Americans across every region of the United States have seen an explosive growth in monthly credit card payments since 2018. Credit card users in the Northeast had their monthly payment increase by nearly 42 percent, followed by 38 percent in the South, over 36 percent in the West, and over 35 percent in the Midwest.

Mapping the Crisis

Across multiple measures, credit card borrowers in the South are struggling the most to make ends meet and pay off their bills.

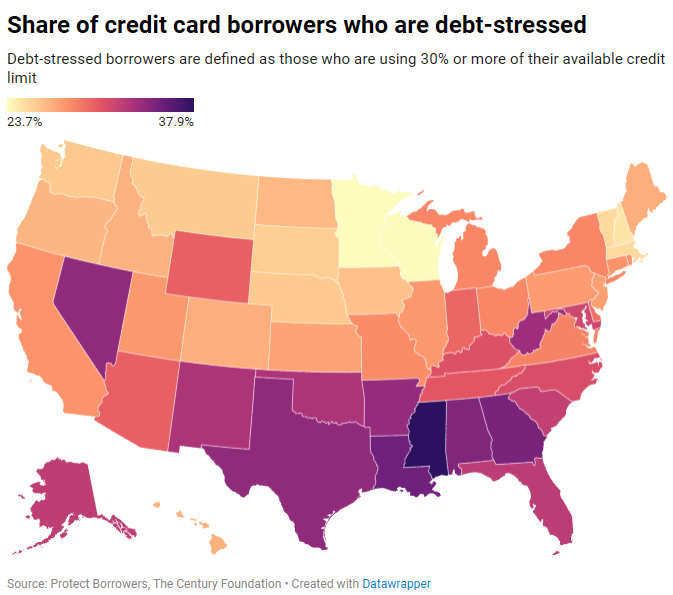

Below is a map of the share of credit card borrowers who are debt-stressed in each state. Debt-stressed borrowers are those who have used up more than 30 percent of their available credit limit, and are highly likely to carry credit card debt from month to month. As a result, they are often exposed to sky-high credit card interest rates which can trap them in persistent debt, and their credit scores (and with it, access to other credit) may spiral downward as a result of both high utilization rates and missed or partial payments. The share of a state’s credit card borrowers who are debt-stressed is a powerful metric that captures how much borrowers are struggling regardless of geographic differences in incomes, costs, spending habits, demographics, etc.

The top five states with the highest share of debt-stressed borrowers are all in the South. They are Mississippi (37.9 percent), Louisiana (35.4 percent), Georgia (35 percent), Alabama (34.7 percent), and Texas (34.2 percent). Moreover, 14 out of the 17 Southern states have a higher share of borrowers who are debt-stressed than the national average (30 percent). Debt-stressed borrowers in the South have also seen their average monthly payments increase from about $850 to $1,150 (over 35 percent) since 2018, the highest of any region.

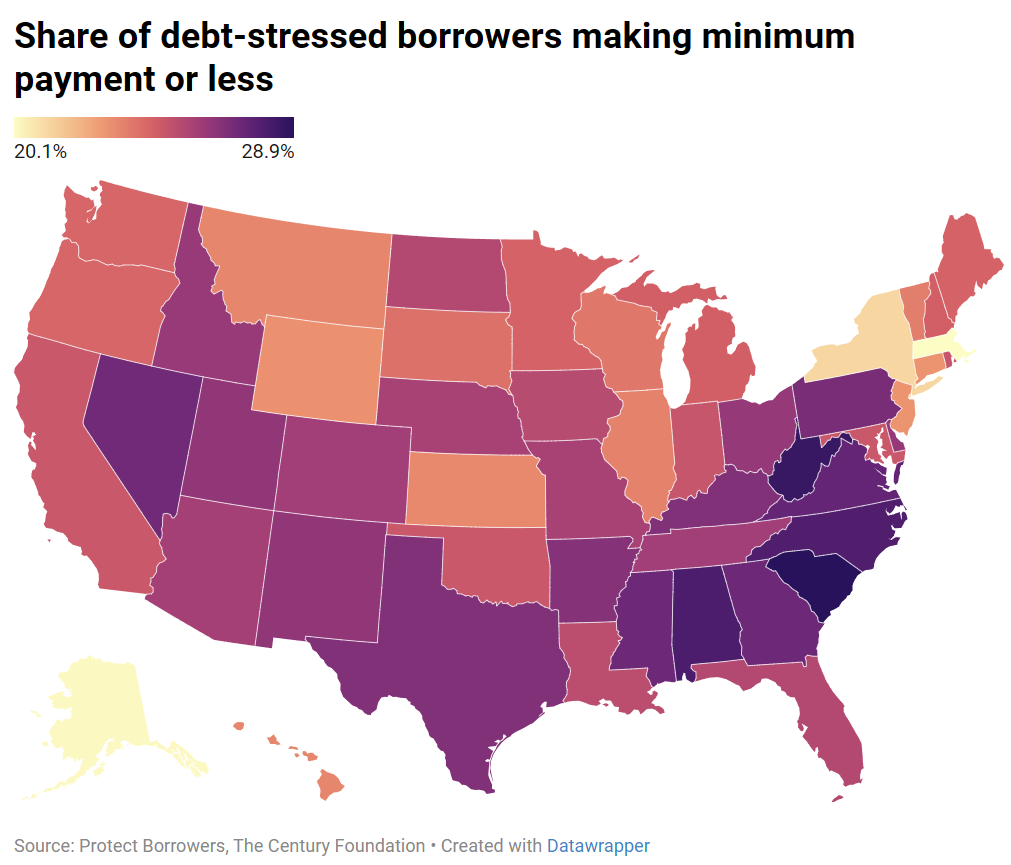

On top of this, debt-stressed borrowers in the South are falling the fastest into high-interest debt. Over 1 in 4 debt-stressed borrowers in the South can only afford to make the minimum payment or less, the highest of any region. This should sound alarm bells for policymakers: minimum payments range from a flat fee of $30 or $40 to just 1 to 3 percent of the total outstanding balance. Borrowers who can only afford the minimum payment are often in financial crisis—they might have just lost their job or been forced to take on a massive amount of debt for an emergency that they may never be able to repay. They’re also far along the road to potentially becoming delinquent on their payments and eventually entering default.

The top seven states where debt-stressed borrowers are only able to make the minimum payment or less are all in the South. Specifically, they include South Carolina (where 28.9 percent of debt-stressed borrowers are making the minimum payment or less), West Virginia (28.5 percent), Alabama (28 percent), North Carolina (27.9 percent), Virginia (27.4 percent), Georgia (27.2 percent), and Mississippi (27.2 percent).

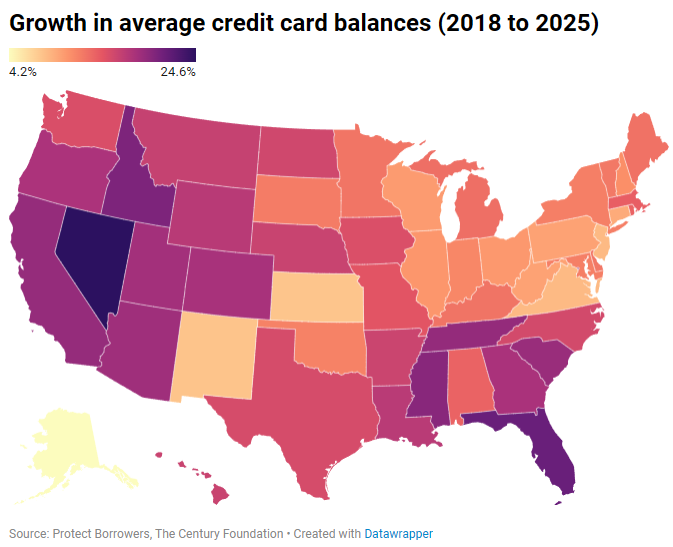

States in the South and West have also seen the largest increases in credit card debt burdens since 2018. Average credit card debt balances increased by over 16 percent in the Western states, followed by more than 15 percent in the South. The states leading the jump are Nevada (24.6 percent), Florida (21.3 percent), Idaho (20.3 percent), Mississippi (19.7 percent), and the District of Columbia (19.2 percent).

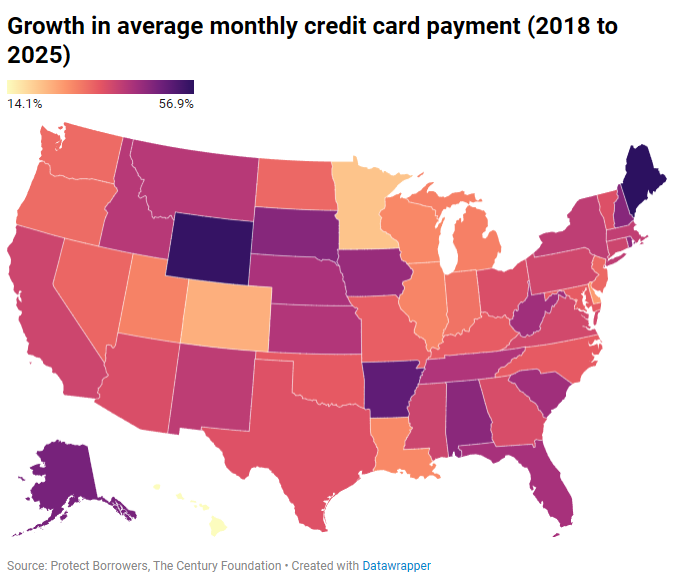

Finally, all states have seen an explosive growth in the amount of borrowers’ paychecks that are going to credit card bills. Borrowers in the Northeast had a nearly 42 percent increase in the size of their average monthly credit card payment, followed by those in the South (38 percent), West (36.2 percent), and Midwest (35.3 percent). The states that led the spike are scattered across the nation, from Maine (56.9 percent) to Wyoming (55.9 percent), Arkansas (51 percent), Alaska (48.5 percent), and South Dakota (46.9 percent).

Broken Promises and a Newfound Love of Inflation

On the campaign trail, President Trump promised to immediately bring prices down, “starting on day one.” A year and a half later, working families are drowning in a worsening affordability crisis, and putting more and more of their paychecks toward paying off debt. Inflation is at a three-year high due to the on-again, off-again tariff war and $4.56-per-gallon gas prices from the ham-fisted Iran War. Millions of families are losing and will lose their SNAP benefits and Medicaid coverage in the coming months. And the massive business conglomerates responsible for price-gouging working families are getting off scot free.

President Donald Trump also made headlines (in many of the states struggling most with credit card debt) by promising to cap credit card interest rates at 10 percent. After a year of silence following his inauguration, he paid lip service to a one-year version of the proposed cap in early 2026, then forgot about it a month later.

When confronted earlier this month with the fact that prices have risen at their fastest rate in three years, President Trump remarked: “I love the inflation.”

Well, so do the credit card banks and other financial companies that are making billions of dollars from pushing working families into debt. When Americans can’t afford the essentials, lenders and financial companies stand to make record profits.

On that front, the Trump Administration has only made it easier for unscrupulous lenders to defraud working people. It obliterated the Consumer Financial Protection Bureau (CFPB), raised costs and reduced competition in the credit card market, and gave multi-billion dollar pardons to credit card banks and other financial institutions that harmed and defrauded millions of Americans. Many of these pardons appear to have been solicited as personal favors by former friends or colleagues of the Trump CFPB’s leadership team, or were given to firms that backed the Trump campaign or donated to his inauguration fund.

While the Trump Administration delivers billion-dollar handouts and favors to banks, working families get broken promises. Americans desperately need relief from record-high interest rates and the crushing weight of credit card debt.

Notes

Geographic divisions of states follow classifications set by the U.S. Census Bureau.

###

Aissa Canchola Bañez is the Policy Director at Protect Borrowers. Previously, Aissa led outreach and engagement efforts for the Office for Students and Young Consumers at the Consumer Financial Protection Bureau and served in senior policy roles in the U.S. House of Representatives and U.S. Senate.

Gerardo Bonilla Chavez is Director of Government Affairs at The Century Foundation. In this capacity, he helps elected officials and staff understand education, health care, and economic public policy, and finds creative ways to implement them. Rooted in the belief that government can and must serve the public good, Gerardo works to advance tangible results for communities too often left behind.

This blog was also published on In Debt, a Protect Borrowers Substack.